Section 230 of the Communications Decency Act has been rightfully called “the twenty-six words that created the Internet.” It is a valuable legal shield which allows internet hosts and platforms the ability to distribute user-generated content and practice moderation without unreasonable fear of being sued, something which forms the basis of all social media, user review, and user forum, and internet hosting services.

While I think it’s reasonable to modify Section 230 to obligate platforms to help victims of clearly heinous acts like cyberstalking, swatting, violent threats, and human rights violations, what the Democratic Senators are proposing goes far beyond that in several dangerous ways.

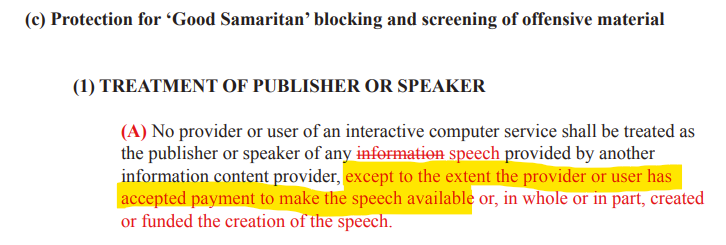

First, Warner and his colleagues have proposed carving out from Section 230 all content which accompanies payment (see below). While I sympathize with what I believe was the intention (to put a different bar on advertisements), this is remarkably short-sighted, because Section 230 applies to far more than companies with ad / content moderation policies Democrats dislike such as Facebook, Google, and Twitter.

It also encompasses email providers, web hosts, user generated review sites, and more. Any service that currently receives payment (for example: a paid blog hosting service, any eCommerce vendor who lets users post reviews, a premium forum, etc) could be made liable for any user posted content. This would make it legally and financially untenable to host any potentially controversial content.

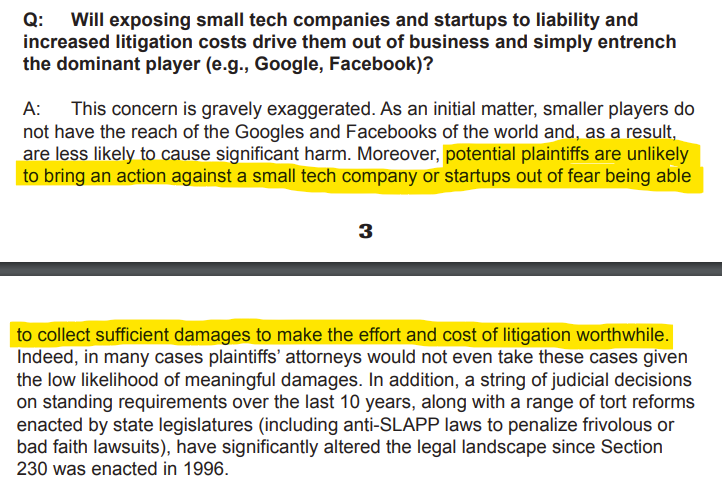

Secondly, these rules will disproportionately impact smaller companies and startups. This is because these smaller companies lack the resources that larger companies have to deal with the new legal burdens and moderation challenges that such a change to Section 230 would call for. It’s hard to know if Senator Warner’s glip answer in his FAQ that people don’t litigate small companies (see below) is ignorance or a willful desire to mislead, but ask tech startups how they feel about patent trolls and whether or not being small protects them from frivolous lawsuits

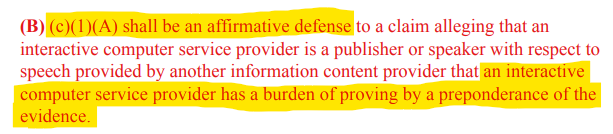

Third, the use of the language “affirmative defense” and “injunctive relief” may have far-reaching consequences that go beyond minor changes in legalese (see below). By reducing Section 230 from an immunity to an affirmative defense, it means that companies hosting content will cease to be able to dismiss cases that clearly fall within Section 230 because they now have a “burden of [proof] by a preponderance of the evidence.”

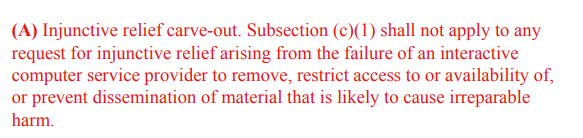

Similarly, carving out “injunctive relief” from Section 230 protections (see below) means that Section 230 doesn’t apply if the party suing is only interested in taking something down (but not financial damages)

I suspect the intention of these clauses is to make it harder for large tech companies to dodge legitimate concerns, but what this practically means is that anyone who has the money to pursue legal action can simply tie up any internet company or platform hosting content that they don’t like.

That may seem like hyperbole, but this is what happened in the UK until 2014 where libel / slander laws making it easy for wealthy individuals and corporations to sue anyone for negative press due to weak protections. Imagine Jeffrey Epstein being able to sue any platform for carrying posts or links to stories about his actions or any individual for forwarding an unflattering email about him.

There is no doubt that we need new tools and incentives (both positive and negative) to tamp down on online harms like cyberbullying and cyberstalking, and that we need to come up with new and fair standards for dealing with “fake news”. But, it is distressing that elected officials will react by proposing far-reaching changes that show a lack of thoughtfulness as it pertains to how the internet works and the positives of existing rules and regulations.

It is my hope that this was only an early draft that will go through many rounds of revisions with people with real technology policy and technology industry expertise.

While it’s impossible to quantify all the intangibles of a college education, the tools of finance offers a practical, quantitative way to look at the tangible costs and benefits which can shed light on (1) whether to go to college / which college to go to, (2) whether taking on debt to pay for college is a wise choice, and (3) how best to design policies around student debt.

The below briefly walks through how finance would view the value of a college education and the soundness of taking on debt to pay for it and how it can help guide students / families thinking about applying and paying for colleges and, surprisingly, how there might actually be too little college debt and where policy should focus to address some of the issues around the burden of student debt.

The Finance View: College as an Investment

Through the lens of finance, the choice to go to college looks like an investment decision and can be evaluated in the same way that a company might evaluate investing in a new factory. Whereas a factory turns an upfront investment of construction and equipment into profits on production from the factory, the choice to go to college turns an upfront investment of cash tuition and missed salary while attending college into higher after-tax wages.

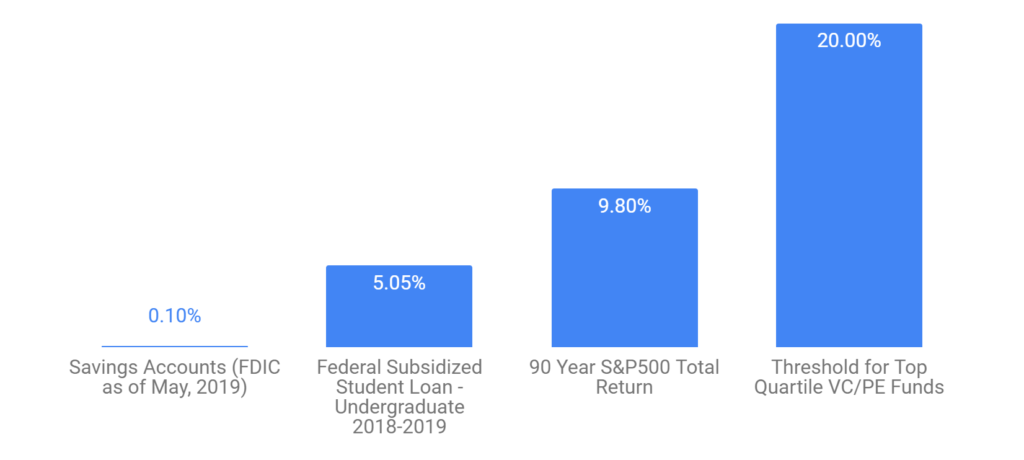

Finance has come up with different ways to measure returns for an investment, but one that is well-suited here is the internal rate of return (IRR). The IRR boils down all the aspects of an investment (i.e., timing and amount of costs vs. profits) into a single percentage that can be compared with the rates of return on another investment or with the interest rate on a loan. If an investment’s IRR is higher than the interest rate on a loan, then it makes sense to use the loan to finance the investment (i.e., borrowing at 5% to make 8%), as it suggests that, even if the debt payments are relatively onerous in the beginning, the gains from the investment will more than compensate for it.

To give an example: if Sally Student can get a starting salary after college in line with the average salary of an 18-24 year old Bachelor’s degree-only holder ($47,551), would have earned the average salary of an 18-24 year old high school diploma-only holder had she not gone to college ($30,696), and expects wage growth similar to what age-matched cohorts saw from 1997-2017, then the IRR of a 4-year degree at a non-profit private school if Sally pays the average net (meaning after subtracting grants and tax credits) tuition, fees, room & board ($26,740/yr in 2017, or a 4-year cost of ~$106,960), the IRR of that investment in college would be 8.1%.

Playing out different scenarios shows which factors are important in determining returns. An obvious factor is the cost of college:

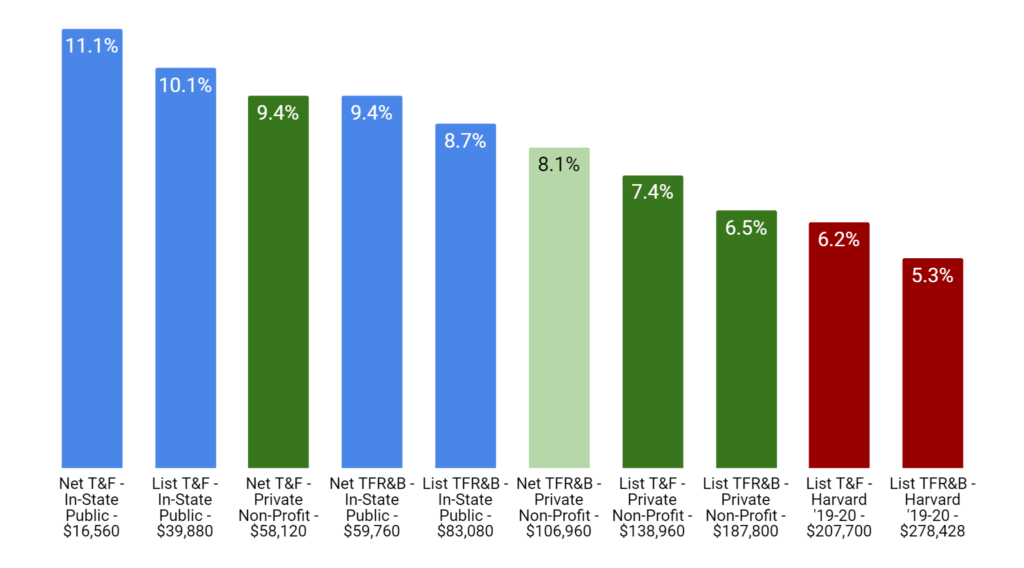

T&F: Tuition & Fees; TFR&B: Tuition, Fees, Room & Board List: Average List Price; Net: Average List Price Less Grants and Tax Benefits Blue: In-State Public; Green: Private Non-Profit; Red: Harvard

As evident from the chart, there is huge difference between the rate of return Sally would get if she landed the same job but instead attended an in-state public school, did not have to pay for room & board, and got a typical level of financial aid (a stock-market-beating IRR of 11.1%) versus the world where she had to pay full list price at Harvard (IRR of 5.3%). In one case, attending college is a fantastic investment and Sally borrowing money to pay for it makes great sense (investors everywhere would love to borrow at ~5% and get ~11%). In the other, the decision to attend college is less straightforward (financially), and it would be very risky for Sally to borrow money at anything near subsidized rates to pay for it.

Some other trends jump out from the chart. Attending an in-state public university improves returns for the average college wage-earner by 1-2% compared with attending private universities (comparing the blue and green bars). Getting an average amount of financial aid (paying net vs list) also seems to improve returns by 0.7-1% for public schools and 2% for private.

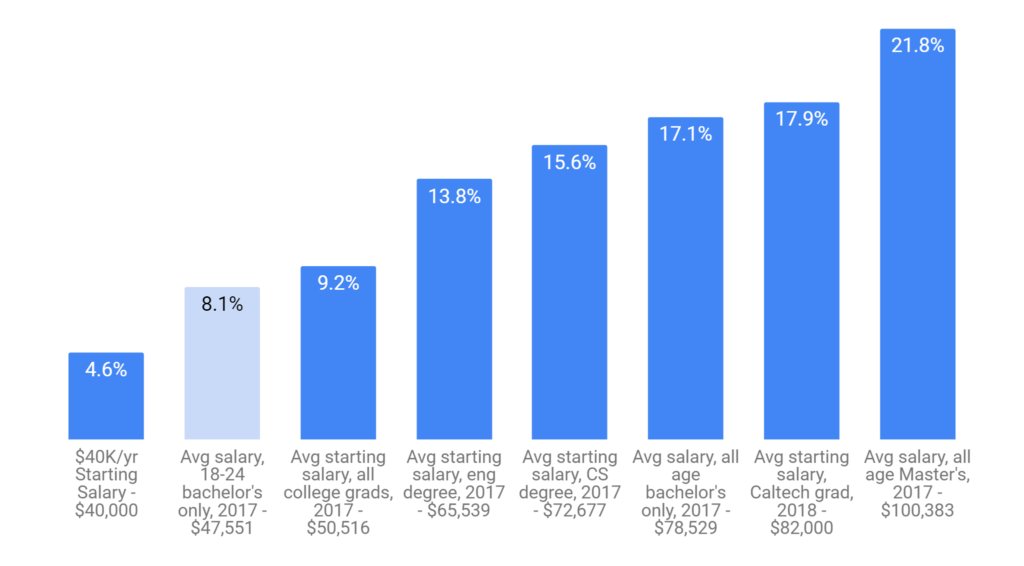

As with college costs, the returns also understandably vary by starting salary:

There is a night and day difference between the returns Sally would see making $40K per year (~$10K more than an average high school diploma holder) versus if she made what the average Caltech graduate does post-graduation (4.6% vs 17.9%), let alone if she were to start with a six-figure salary (IRR of over 21%). If Sally is making six figures, she would be making better returns than the vast majority of venture capital firms, but if she were starting at $40K/yr, her rate of return would be lower than the interest rate on subsidized student loans, making borrowing for school financially unsound.

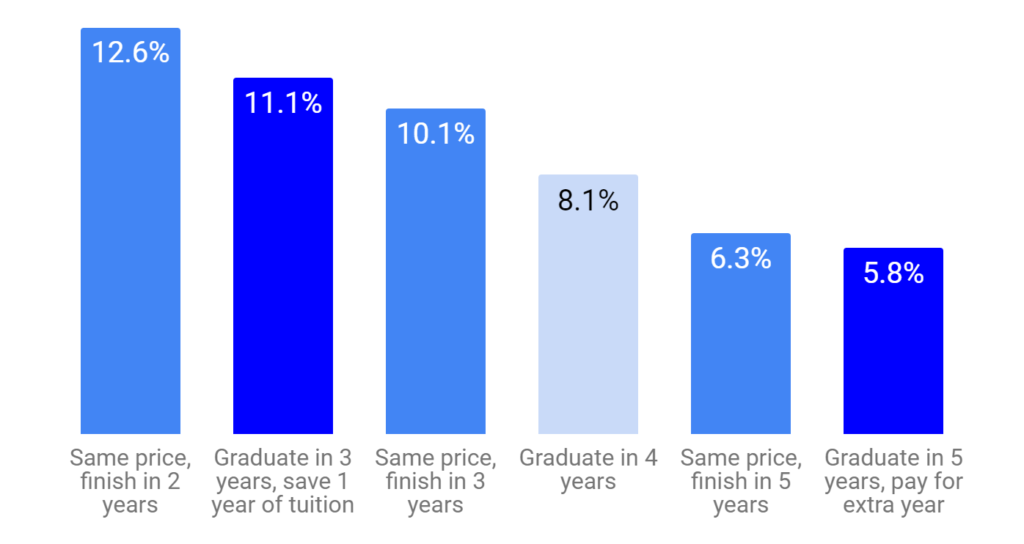

Time spent in college also has a big impact on returns:

Graduating sooner not only reduces the amount of foregone wages, it also means earning higher wages sooner and for more years. As a result, if Sally graduates in two years while still paying for four years worth of education costs, she would experience a higher return (12.6%) than if she were to graduate in three years and save one year worth of costs (11.1%)! Similarly, if Sally were to finish school in five years instead of four, this would lower her returns (6.3% if still only paying for four years, 5.8% if adding an extra year’s worth of costs). The result is that an extra / less year spent in college is a ~2% hit / boost to returns!

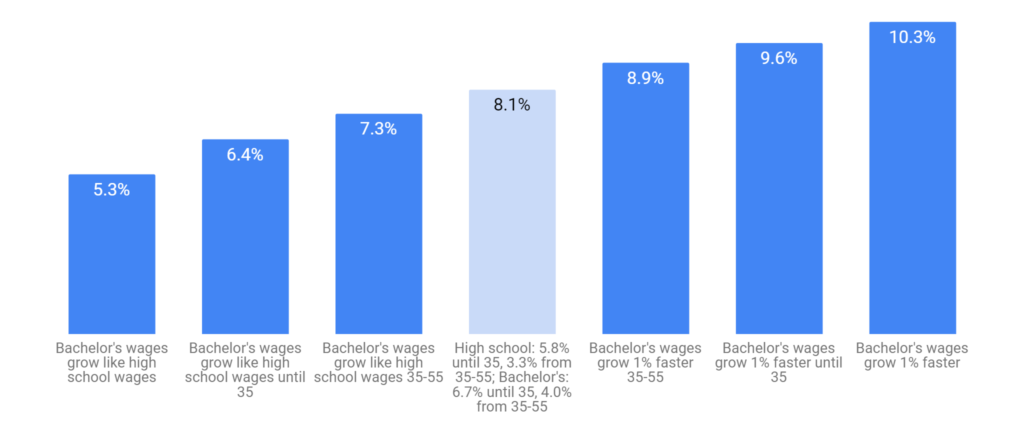

Finally, how quickly a college graduate’s wages growrelative to a high school diploma holder’s also has a significant impact on the returns to a college education:

Census/BLS data suggests that, between 1997 and 2017, wages of bachelor’s degree holders grew faster on an annualized basis by ~0.7% per year than for those with only a high school diploma (6.7% vs 5.8% until age 35, 4.0% vs 3.3% for ages 35-55, both sets of wage growth appear to taper off after 55).

The numbers show that if Sally’s future wages grew at the same rate as the wages of those with only a high school diploma, her rate of return drops to 5.3% (just barely above the subsidized loan rate). On the other hand, if Sally’s wages end up growing 1% faster until age 55 than they did for similar aged cohorts from 1997-2017, her rate of return jumps to a stock-market-beating 10.3%.

Lessons for Students / Families

What do all the charts and formulas tell a student / family considering college and the options for paying for it?

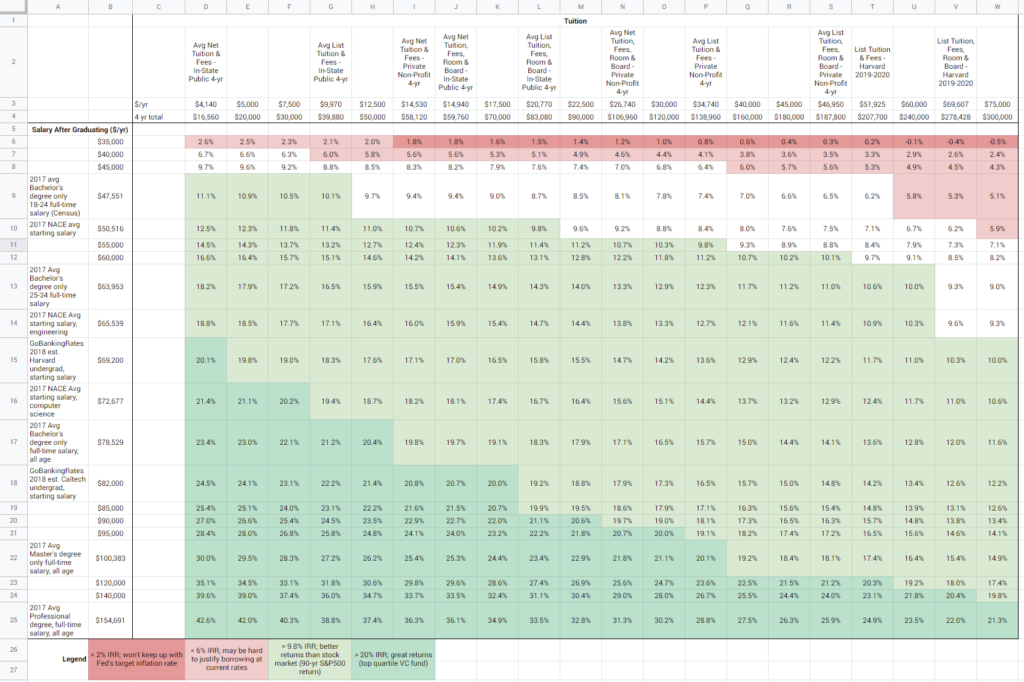

First, college can be an amazing investment, well worth taking on student debt and the effort to earn grants and scholarships. While there is well-founded concern about the impact that debt load and debt payments can have on new graduates, in many cases, the financial decision to borrow is a good one. Below is a sensitivity table laying out the rates of return across a wide range of starting salaries (the rows in the table) and costs of college (the columns in the table) and color codes how the resulting rates of return compare with the cost of borrowing and with returns in the stock market (red: risky to borrow at subsidized rates; white: does make sense to borrow at subsidized rates but it’s sensible to be mindful of the amount of debt / rates; green: returns are better than the stock market).

Except for graduates with well below average starting salaries (less than or equal to $40,000/yr), most of the cells are white or green. At the average starting salary, except for those without financial aid attending a private school, the returns are generally better than subsidized student loan rates. For those attending public schools with financial aid, the returns are better than what you’d expect from the stock market.

Secondly, there are ways to push returns to a college education higher. They involve effort and sometimes painful tradeoffs but, financially, they are well worth considering. Students / families choosing where to apply or where to go should keep in mind costs, average starting salaries, quality of career services, and availability of financial aid / scholarships / grants, as all of these factors will have a sizable impact on returns. After enrollment, student choices / actions can also have a meaningful impact: graduating in fewer semesters/quarters, taking advantage of career resources to research and network into higher starting salary jobs, applying for scholarships and grants, and, where possible, going for a 4th/5th year masters degree can all help students earn higher returns to help pay off any debt they take on.

Lastly, use the spreadsheet*! The figures and charts above are for a very specific set of scenarios and don’t factor in any particular individual’s circumstances or career trajectory, nor is it very intelligent about selecting what the most likely alternative to a college degree would be. These are all factors that are important to consider and may dramatically change the answer.

*To use the Google Sheet, you must be logged into a Google account; use the “Make a Copy” command in the File menu to save a version to your Google Drive and edit the tan cells with red numbers in them to whatever best matches your situation and see the impact on the yellow highlighted cells for IRR and the age when investment pays off

Implications for Policy on Student Debt

Given the growing concerns around student debt and rising tuitions, I went into this exercise expecting to find that the rates of return across the board would be mediocre for all but the highest earners. I was (pleasantly) surprised to discover that a college graduate earning an average starting salary would be able to achieve a rate of return well above federal loan rates even at a private (non-profit) university.

While the rate of return is not a perfect indicator of loan affordability (as it doesn’t account for how onerous the payments are compared to early salaries), the fact that the rates of return are so high is a sign that, contrary to popular opinion, there may actually be too little student debt rather than too much, and that the right policy goal may actually be to find ways to encourage the public and private sector to make more loans to more prospective students.

As for concerns around affordability, while proposals to cancel all student debt plays well to younger voters, the fact that many graduates are enjoying very high returns suggests that such a blanket policy is likely unnecessary, anti-progressive (after all, why should the government zero out the costs on high-return investments for the soon-to-be upper and upper-middle-classes), and fails to address the root cause of the issue (mainly that there shouldn’t be institutions granting degrees that fail to be good financial investments). Instead, a more effective approach might be:

Require all institutions to publish basic statistics (i.e. on costs, availability of scholarships/grants, starting salaries by degree/major, time to graduation, etc.) to help students better understand their own financial equation

Hold educational institutions accountable when too many students graduate with unaffordable loan burdens/payments (i.e. as a fraction of salary they earn and/or fraction of students who default on loans) and require them to make improvements to continue to qualify for federally subsidized loans

Making it easier for students to discharge student debt upon bankruptcy and increasing government oversight of collectors / borrower rights to prevent abuse

Government-supported loan modifications (deferrals, term changes, rate modifications, etc.) where short-term affordability is an issue (but long-term returns story looks good); loan cancellation in cases where debt load is unsustainable in the long-term (where long-term returns are not keeping up) or where debt was used for an institution that is now being denied new loans due to unaffordability

Making the path to public service loan forgiveness (where graduates who spend 10 years working for non-profits and who have never missed an interest payment get their student loans forgiven) clearer and addressing some of the issues which have led to 99% of applications to date being rejected

Special thanks Sophia Wang, Kathy Chen, and Dennis Coyle for reading an earlier version of this and sharing helpful comments!

There’s been a fair amount of talk lately about proactively regulating — and maybe even breaking up — the “Big Tech” companies.

Full disclosure: this post discusses regulating large tech companies. I own shares in several of these both directly (in the case of Facebook and Microsoft) and indirectly (through ETFs that own stakes in large companies)

Like many, I have become increasingly uneasy over the fact that a small handful of companies, with few credible competitors, have amassed so much power over our personal data and what information we see. As a startup investor and former product executive at a social media startup, I can especially sympathize with concerns that these large tech companies have created an unfair playing field for smaller companies.

At the same time, though, I’m mindful of all the benefits that the tech industry — including the “tech giants” — have brought: amazing products and services, broader and cheaper access to markets and information, and a tremendous wave of job and wealth creation vital to may local economies. For that reason, despite my concerns of “big tech”‘s growing power, I am wary of reaching for “quick fixes” that might change that.

Another factor which complicates tech policy is that the traditional “big is bad” mentality ignores the benefits to having large platforms. While Amazon’s growth has hurt many brick & mortar retailers and eCommerce competitors, its extensive reach and infrastructure enabled businesses like Anker and Instant Pot to get to market in a way which would’ve been virtually impossible before. While the dominance of Google’s Android platform in smartphones raised concerns from European regulators, its hard to argue that the companies which built millions of mobile apps and tens of thousands of different types of devices running on Android would have found it much more difficult to build their businesses without such a unified software platform. Policy aimed at “Big Tech” should be wary of dismantling the platforms that so many current and future businesses rely on.

Its also important to remember that poorly crafted regulation in tech can be self-defeating. The most effective way to deal with the excesses of “Big Tech”, historically, has been creating opportunities for new market entrants. After all, many tech companies previously thought to be dominant (like Nokia, IBM, and Microsoft) lost their positions, not because of regulation or antitrust, but because new technology paradigms (i.e. smartphones, cloud), business models (i.e. subscription software, ad-sponsored), and market entrants (i.e. Google, Amazon) had the opportunity to flourish. Because rules (i.e. Article 13/GDPR) aimed at big tech companies generally fall hardest on small companies (who are least able to afford the infrastructure / people to manage it), its important to keep in mind how solutions for “Big Tech” problems affect smaller companies and new concepts as well.

To be 100% clear, I’m not saying that the tech industry and big platforms should be given a pass on rules and regulation. If anything, I believe that laws and regulation play a vital role in creating flourishing markets.

But, instead of treating “Big Tech” as just a problem to kill, I think we’d be better served by laws / regulations that recognize the limits of regulation on tech and, instead, focus on making sure emerging companies / technologies can compete with the tech giants on a level playing field. To that end, I hope to see more ideas that embrace the following four pillars:

I. Tiering regulation based on size of the company

Regulations on tech companies should be tiered based on size with the most stringent rules falling on the largest companies. Size should include traditional metrics like revenue but also, in this age of marketplace platforms and freemium/ad-sponsored business models, account for the number of users (i.e. Monthly Active Users) and third party partners.

In this way, the companies with the greatest potential for harm and the greatest ability to bear the costs face the brunt of regulation, leaving smaller companies & startups with greater flexibility to innovate and iterate.

II. Championing data portability

One of the reasons it’s so difficult for competitors to challenge the tech giants is the user lock-in that comes from their massive data advantage. After all, how does a rival social network compete when a user’s photos and contacts are locked away inside Facebook?

While Facebook (and, to their credit, some of the other tech giants) does offer ways to export user data and to delete user data from their systems, these tend to be unwieldy, manual processes that make it difficult for a user to bring their data to a competing service. Requiring the largest tech platforms to make this functionality easier to use (i.e., letting others import your contact list and photos with the ease in which you can login to many apps today using Facebook) would give users the ability to hold tech companies accountable for bad behavior or not innovating (by being able to walk away) and fosters competition by letting new companies compete not on data lock-in but on features and business model.

I believe that is an overreaction. Platform owners offering attractive products and services (i.e., Google offering turn-by-turn navigation on Android phones) can be a great thing for users (after all, most prominent platforms started by providing compelling first-party offerings) and for 3rd party participants if these offerings improve the attractiveness of the platform overall.

What is hard to justify is when platform owners stack the deck in their favor using anti-competitive moves such as banning or reducing the visibility of competitors,crippling third party offerings, making excessive demands on 3rd parties, etc. Its these sorts of actions by the largest tech platforms that pose a risk to consumer choice and competition and should face regulatory scrutiny. Not just the fact that a large platform exists or that the platform owner chooses to participate in it.

IV. Modernizing how anti-trust thinks about defensive acquisitions

The rise of the tech giants has led to many calls to unwind some of the pivotal mergers and acquisitions in the space. As much as I believe that anti-trust regulators made the wrong calls on some of these transactions, I am not convinced, beyond just wanting to punish “Big Tech” for being big, that the Pandora’s Box of legal and financial issues (for the participants, employees, users, and for the tech industry more broadly) that would be opened would be worthwhile relative to pursuing other paths to regulate bad behavior directly.

That being said, its become clear that anti-trust needs to move beyond narrow revenue share and pricing-based definitions of anti-competitiveness (which do not always apply to freemium/ad-sponsored business models). Anti-trust prosecutors and regulators need to become much more thoughtful and assertive around how some acquisitions are done simply to avoid competition (i.e., Google’s acquisition of Waze and Facebook’s acquisition of WhatsApp are two examples of landmark acquisitions which probably should have been evaluated more closely).

This is hardly a complete set of rules and policies needed to approach growing concerns about “Big Tech”. Even within this framework, there are many details (i.e., who the specific regulators are, what specific auditing powers they have, the details of their mandate, the specific thresholds and number of tiers to be set, whether pre-installing an app counts as unfair, etc.) that need to be defined which could make or break the effort. But, I believe this is a good set of principles that balances both the need to foster a tech industry that will continue to grow and drive innovation as well as the need to respond to growing concerns about “Big Tech”.

Special thanks to Derek Yang and Anthony Phan for reading earlier versions and giving me helpful feedback!