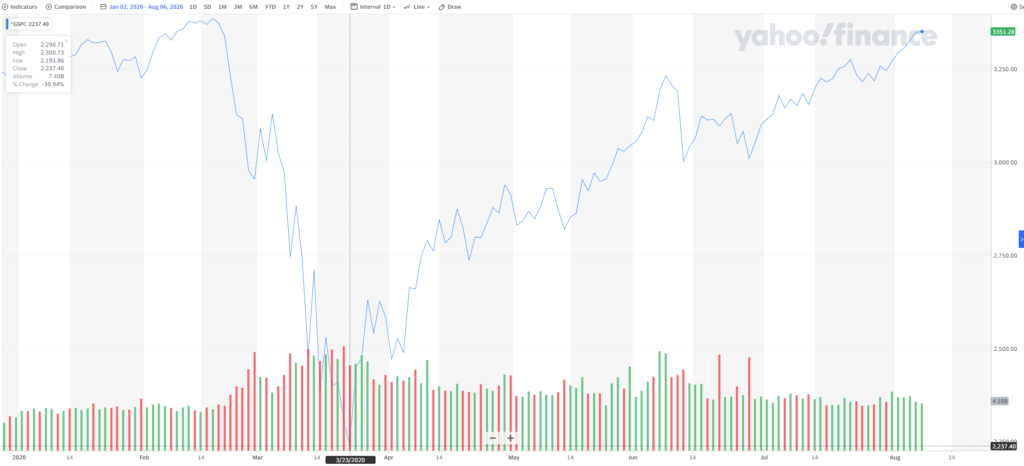

The fires in Maui have had a devastating human toll (111 dead, 1000 missing as of this writing). It is not surprising that it’s raising some questions about the role of Hawaii’s utility (Hawaiian Electric/HECO) played in the disaster.

Utilities now face three simultaneous problems (arguably of their own making):

climate change escalating the risks of catastrophic wildfires and storms

utilities across the country having aging energy infrastructure

homeownership patterns, disaster insurance coverage & premiums, and utility risk management plans built for a pre-climate-change risk environment

The smart ones will be proactively overhauling their processes and infrastructure to cope with this. The less smart ones will potentially be dragged kicking and screaming into this world in much the same way that PG&E and Hawaiian Electric currently are.

Hawaiian Electric is speaking with firms that specialize in restructuring advisory work, exploring options to address the electric utility’s financial and legal challenges arising from the Maui wildfires, said people familiar with the matter.

Hawaiian Electric is facing a selloff in its stock and bonds, and has been hit with lawsuits alleging that its actions both before and during the wildfires exacerbated the devastation Maui residents have suffered.

using Pihole as a local DNS server to have custom web addresses for software services running on your network and Nginx to handle port forwarding

Twingate (a better alternative to opening up a port and setting up Dynamic DNS to grant secure access to your network)

Pihole

Pihole is a lightweight localDNS server (it gets its name from the Raspberry Pi, a <$100 device popular with hobbyists, that it can run fully on).

A DNS (or Domain Name Server) converts human readable addresses (like www.google.com) into IP addresses (like 142.250.191.46). As a result, every piece of internet-connected technology is routinely making DNS requests when using the internet. Internet service providers typically offer their own DNS servers for their customers. But, some technology vendors (like Google and CloudFlare) also offer their own DNS services with optimizations on speed, security, and privacy.

A home-grown DNS server like Pihole can layer additional functionality on top:

DNS “filter” for ad / tracker blocking: Pihole can be configured to return dummy IP addresses for specific domains. This can be used to block online tracking or ads (by blocking the domains commonly associated with those activities). While not foolproof, one advantage this approach has over traditional ad blocking software is that, because this blocking happens at the network level, the blocking extends to all devices on the network (such as internet-connected gadgets, smart TVs, and smartphones) without needing to install any extra software.

DNS caching for performance improvements: In addition to the performance gains from blocking ads, Pihole also boosts performance by caching commonly requested domains, reducing the need to “go out to the internet” to find a particular IP address. While this won’t speed up a video stream or download, it will make content from frequently visited sites on your network load faster by skipping that internet lookup step.

Login to your OpenMediaVault web admin panel, go to [Services > Compose > Files], and press the button. Under Name put down Pihole and under File, adapt the following (making sure the number of spaces are consistent)

version: "3" services: pihole: container_name: pihole image: pihole/pihole:latest ports: - "53:53/tcp" - "53:53/udp" - "8000:80/tcp" environment: TZ: 'America/Los_Angeles' WEBPASSWORD: '<Password for the web admin panel>' FTLCONF_LOCAL_IPV4: '<your server IP address>' volumes: - '<absolute path to shared config folder>/pihole:/etc/pihole' - '<absolute path to shared config folder>/dnsmasq.d:/etc/dnsmasq.d' restart: unless-stopped

You’ll need to replace <Password for the web admin panel> with the password you’ll want to use to be access the Pihole web configuration interface, <your server IP address> with the static local IP address for your server, and <absolute path to shared config folder> with the absolute path to the config folder where you want Docker-installed applications to store their configuration information (accessible by going to [Storage > Shared Folders] in the administrative panel).

I live in the Bay Area so I set timezone TZ to America/Los_Angeles. You can find yours here.

Under Ports, I’ve kept the port 53 reservation (as this is the standard port for DNS requests) but I’ve chosen to map the Pihole administrative console to port 8000 (instead of the default of port 80 to avoid a conflict with the OpenMediaVault admin panel default). Note: This will prevent you from using Pihole’s default pi.hole domain as a way to get to the Pihole administrative console out-of-the-box. Because standard web traffic goes to port 80 (and this configuration has Pihole listening at port 8080), pi.hole would likely just direct you to the OpenMediaVault panel. While you could let pi.hole take over port 80, you would need to move OpenMediaVault’s admin panel to a different port (which itself has complexity). I ultimately opted with keeping OpenMediaVault at port 80 knowing that I could configure Pihole and Nginx proxy (see below) to redirect pi.hole to the right port.

You’ll notice this configures two volumes, one for dnsmasq.d, which is the DNS service, and one for pihole which provides an easy way to configure dnsmasq.d and download blocklists.

Note: the above instructions assume your home network, like most, is IPv4 only. If you have an IPv6 network, you will need to add an IPv6: True line under environment: and replace the FTLCONF_LOCAL_IPV4:'<server IPv4 address>' with FTLCONF_LOCAL_IPV6:'<server IPv6 address>'. For more information, see the official Pihole Docker instructions.

Once you’re done, hit Save and you should be returned to your list of Docker compose files for the next step. Notice that the new Pihole entry you created has a Down status, showing the container has yet to be initiated.

Disabling systemd-resolved: Most modern Linux operating systems include a built-in DNS resolver that listens on port 53 called systemd-resolved. Prior to initiating the Pihole container, you’ll need to disable this to prevent that port conflict. Use WeTTy (refer to the section Docker and OMV-Extras in my previous post) or SSH to login as the root user to your OpenMediaVault command line. Enter the following command:

nano /etc/systemd/resolved.conf

Look for the line that says #DNSStubListener=yes and replace it with DNSStubListener=no, making sure to remove the # at the start of the line. (Hit Ctrl+X to exit, Y to save, and Enter to overwrite the file). This configuration will tell systemd-resolved to stop listening to port 53.

To complete the configuration change, you’ll need to edit the symlink /etc/resolv.conf to point to the file you just edited by running:

sh -c 'rm /etc/resolv.conf && ln -s /etc/systemd/resolved.conf /etc/resolv.conf'

Now all that remains is to restart systemd-resolved:

systemctl restart systemd-resolved

How to start / update / stop / remove your Pihole container: You can manage all of your Docker Compose files by going to [Services > Compose > Files] in the OpenMediaVault admin panel. Click on the Pihole entry (which should turn it yellow) and press the (up) button. This will create the container, download any files needed, and, if you properly disabled systemd-resolved in the last step, initiate Pihole.

And that’s it! To prove it worked, go to your-server-ip:8000 in a browser and you should see the login for the Pihole admin webpage (see below). From time to time, you’ll want to update the container. OMV makes this very easy. Every time you press the (pull) button in the [Services > Compose > Files] interface, Docker will pull the latest version (maintained by the Pihole team).

Now that you have Pihole running, it is time to enable and configure it for your network.

Test Pihole from a computer: Before you change your network settings, it’s a good idea to make sure everything works.

On your computer, manually set your DNS service to your Pihole by putting in your server IP address as the address for your computer’s primary DNS server (Mac OS instructions; Windows instructions; Linux instructions). Be sure to leave any alternate / secondary addresses blank (many computers will issue DNS requests to every server they have on their list and if an alternative exists you may not end up blocking anything).

(Temporarily) disable any ad blocking service you may have on your computer / browser you want to test with (so that this is a good test of Pihole as opposed to your ad blocking software). Then try to go to https://consumerproductsusa.com/ — this is a URL that is blocked by default by Pihole. If you see a very spammy website promising rewards, either your Pihole does not work or you did not configure your DNS correctly.

Finally login to the Pihole configuration panel (your-server-ip:8000) using the password you set up during installation. From the dashboard click on the Queries Blocked box at the top (your colors may vary but it’s the red box on my panel, see below). On the next screen, you should see the domain consumerproductsusa.com next to the IP address of your computer, confirming that the address was blocked. You can now turn your ad blocking software back on!

You should now set the DNS service on your computer back to “automatic” or “DHCP” so that it will inherit its DNS settings from the network/router (and especially if this is a laptop that you may use on another network).

Configure DNS on router: Once you’ve confirmed that the Pihole service works, you should configure the default DNS settings on your router to make Pihole the DNS service for your entire network. The instructions for this will vary by router manufacturer. If you use Google Wifi as I do, here are the instructions.

Once this is completed, every device which inherits DNS settings from the router will now be using Pihole for their DNS requests.

Note: one downside of this approach is that the Pihole becomes a single point of failure for the entire network. If the Pihole crashes or fails, for any reason, none of your network’s DNS requests will go through until the router’s settings are changed or the Pihole becomes functional again. Pihole generally has good reliability so this is unlikely to be an issue most of the time, but I am currently using Google’s DNS as a fallback on my Google Wifi (for the times when something goes awry with my server) and I would also encourage you to know how to change the DNS settings for your router in case things go bad so that your access to the internet is not taken out unnecessarily.

Configure Pihole: To get the most out of Pihole’s ad blocking functionality, I would suggest three things

Select Good Upstream DNS Servers: From the Pihole administrative panel, click on Settings. Then select the DNS tab. Here, Pihole allows you to configure which external DNS services the DNS requests on your network should go to if they aren’t going to be blocked and haven’t yet been cached. I would recommend selecting the checkboxes next to Google and Cloudflare given their reputations for providing fast, secure, and high quality DNS services (and selecting multiple will provide redundancy).

Update Gravity periodically: Gravity is the system by which Pihole updates its list of domains to block. From the Pihole administrative panel, click on [Tools > Update Gravity] and click the Update button. If there are any updates to the blocklists you are using, these will be downloaded and “turned on”.

Configure Domains to block/allow: Pihole allows administrators to granularly customize the domains to block (blacklist) or allow (whitelist). From the Pihole administrative panel, click on Domains. Here, an admin can add a domain (or a regular expression for a family of domains) to the blacklist (if it’s not currently blocked) or the whitelist (if it currently is) to change what happens when a user on the network accesses the DNS.

I added whitelist exclusions for link.axios.com to let me click through links from the Axios email newsletters I receive and www.googleadservices.com to let my wife click through Google-served ads. Pihole also makes it easy to manually take a domain that a device on your network has requested to block/allow. Tap on Total Queries from the Pihole dashboard, click on the IP address of the device making the request, and you’ll see every DNS request (including those which were blocked) with a link beside them to add to the domain whitelist or blacklist.

Pihole will also allow admins to configure different rules for different sets of devices. This can be done by calling out clients (which can be done by clicking on Clients and picking their IP address / MAC address / hostnames), assigning them to groups (which can be defined by clicking on Groups), and then configuring domain rules to go with those groups (in Domains). Unfortunately because Google Wifi simply forwards DNS requests rather than distributes them, I can only do this for devices that are configured to directly point at the Pihole, but this could be an interesting way to impose parental internet controls.

Now you have a Pihole network-level ad blocker and DNS cache!

Local DNS and Nginx proxy

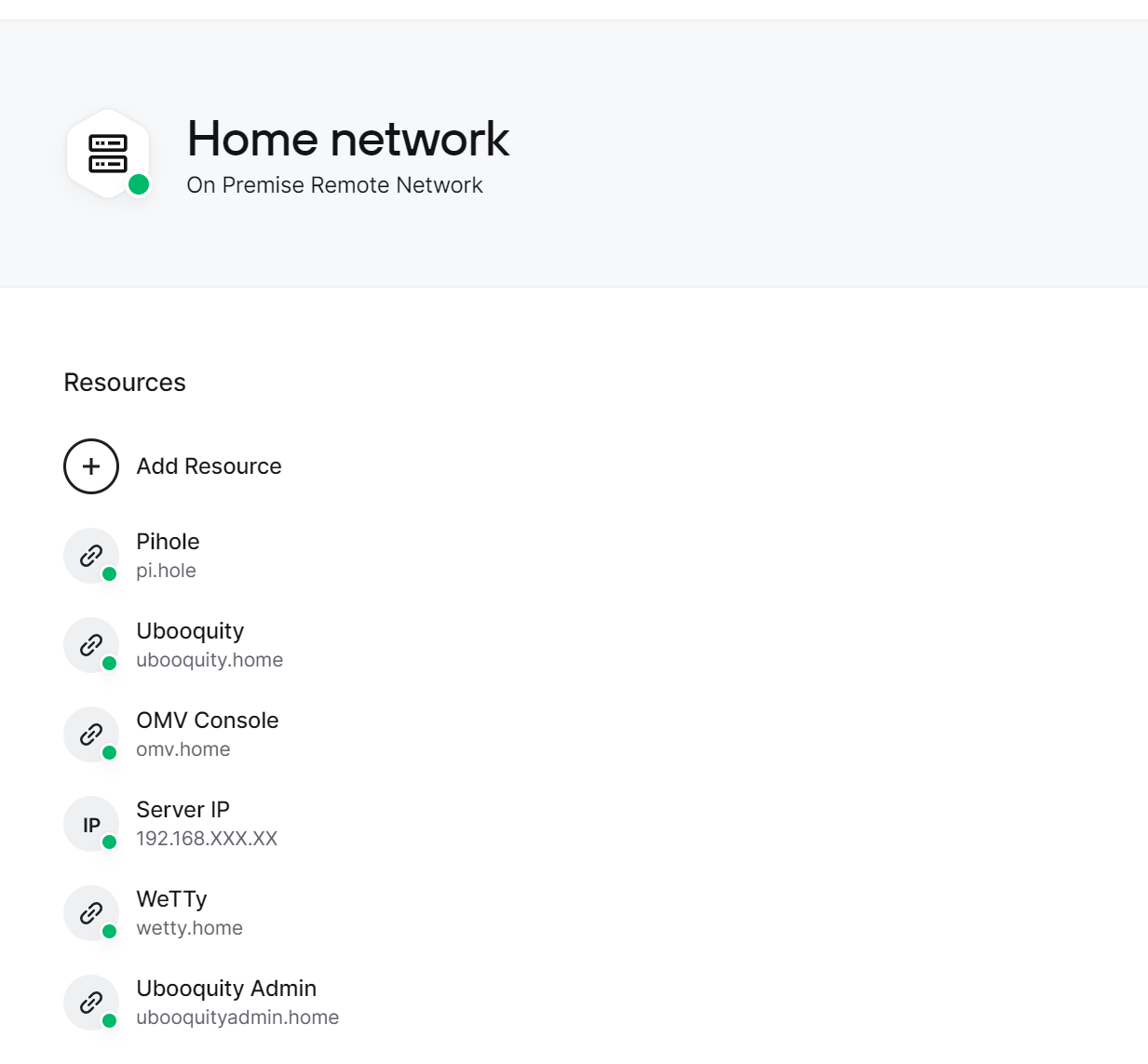

As a local DNS server, Pihole can do more than just block ads. It also lets you create human readable addresses for services running on your network. In my case, I created one for the OpenMediaVault admin panel (omv.home), one for WeTTy (wetty.home), and one for Ubooquity (ubooquity.home).

If your setup is like mine (all services use the same IP address but different ports), you will need to set up a proxy as DNS does not handle port forwarding. Luckily, OpenMediaVault has Nginx, a popular web server with a performant proxy, built-in. While many online tutorials suggest installing Nginx Proxy Manager, that felt like overkill, so I decided to configure Nginx directly.

To get started:

Configure the A records for the domains you want in Pihole: Login to your Pihole administrative console (your-server-ip:8000) and click on [Local DNS > DNS Records] from the sidebar. Under the section called Add a new domain/IP combination, fill out the Domain: you want for a given service (like omv.home or wetty.home) and the IP Address: (if you’ve been following my guides, this will be your-server-ip). Press the Add button and it will show up below. Repeat for all the domains you want. If you have a setup similar to mine, you will see many domains pointed at the same IP address (because the different services are simply different ports on my server).

To test if these work, enter any of the domains you just put in to a browser and it should take you to the login page for the OpenMediaVault admin panel (as currently they are just pointing at your server IP address).

Note 1: while you can generally use whatever domains you want, it is suggested that you don’t use a TLD that could conflict with an actual website (i.e. .com) or that are commonly used by networking systems (i.e. .local or .lan). This is why I used .home for all of my domains (the IETF has a list they recommend, although it includes .lan which I would advise against as some routers such as Google Wifi use this)

Note 2: Pihole itself automatically tries to forward pi.hole to its web admin panel, so you don’t need to configure that domain. The next step (configuring proxy port forwarding) will allow pi.hole to work.

Edit the Nginx proxy configuration: Pihole’s Local DNS server will send users looking for one of the domains you set up (i.e. wetty.home) to the IP address you configured. Now you need your server to forward that request to the appropriate port to get to the right service.

You can do this by taking advantage of the fact that Nginx, by default, will load any .conf file in the /etc/nginx/conf.d/ directory as a proxy configuration. Pick any file name you want (I went with dothome.conf because all of my service domains end with .home) and after using WeTTy or SSH to login as root, run:

nano /etc/nginx/conf.d/<your file name>.conf

The first time you run this, it will open up a blank file. Nginx looks at the information in this file for how to redirect incoming requests. What we’ll want to do is tell Nginx that when a request comes in for a particular domain (i.e. ubooquity.home or pi.hole) that request should be sent to a particular IP address and port.

Manually writing these configuration files can be a little daunting and, truth be told, the text file I share below is the result of a lot of trial and error, but in general there are 2 types of proxy commands that are relevant for making your domain setup work.

One is a proxy_pass where Nginx will basically take any traffic to a given domain and just pass it along (sometimes with additional configuration headers). I use this below for wetty.home, pi.hole, ubooquityadmin.home, and ubooquity.home. It worked without the need to pass any additional headers for WeTTy and Ubooquity, but for pi.hole, I had to set several additional proxy headers (which I learned from this post on Reddit).

The other is a 301 redirect where you tell the client to simply forward itself to another location. I use this for ubooquityadmin.home because the actual URL you need to reach is not / but /admin/ and the 301 makes it easy to setup an automatic forward. I then use the regex match ~ /(.*)$ to make sure every other URL is proxy_pass‘d to the appropriate domain and port.

You’ll notice I did not include the domain I configured for my OpenMediaVault console (omv.home). That is because omv.home already goes to the right place without needing any proxy to port forward.

If you are using other domains, ports, or IP addresses, adjust accordingly. Be sure all your curly braces have their mates ({}) and that each line ends with a semicolon (;) or Nginx will crash. I use Tab‘s between statements (i.e. between listen and 80) to format them more nicely but Nginx will accept any number or type of whitespace.

To test if your new configuration worked, save your changes (hit Ctrl+X to exit, Y to save, and Enter to overwrite the file if you are editing a pre-edited one). In the command line, run the following command to restart Nginx with your new configuration loaded.

systemctl restart nginx

Try to login to your OpenMediaVault administrative panel in a browser. If that works, it means Nginx is up and running and you at least didn’t make any obvious syntax errors!

Next try to access one of the domains you just configured (for instance pi.hole) to test if the proxy was configured correctly.

If either of those steps failed, use WeTTy or SSH to log back in to the command line and use the command above to edit the file (you can delete everything if you want to start fresh) and rerun the restart command after you’ve made changes to see if that fixes it. It may take a little bit of doing if you have a tricky configuration but once you’re set, everyone on the network can now use your configured addresses to access the services on your network.

The work required to set up each device for Wireguard is quite involved (you have to configure it on the VPN server and then pass credentials to the device via QR code or file)

It requires me to open up a port on my router for external traffic (a security risk) and maintain a Dynamic DNS setup that is vulnerable to multiple points of failure and could make changing domain providers difficult.

Simple graphical configuration of which resources should be made available to which devices

Easier to use client software with secure (but still easy to use) authentication

No need to configure Dynamic DNS or open a port

Support for local DNS rules (i.e. the domains I configured in Pihole)

I was intrigued (it didn’t hurt that Twingate has a generous free Starter plan that should work for most home server setups). To set up Twingate to enable remote access:

Create a Twingate account and Network: Go to their signup page and create an account. You will then be asked to set up a unique Network name. The resulting address, <yournetworkname>.twingate.com, will be your Network configuration page from where you can configure remote access.

Add a Remote Network: Click the Add button on the right-hand-side of the screen. Select On Premise for Location and enter any name you choose (I went with Home network).

Add Resources: Select the Remote Network you just created (if you haven’t already) and use the Add Resource button to add an individual domain name or IP address and then grant access to a group of users (by default, it will go to everyone).

With my configuration, I added 5 domains (pi.hole + the four .home domains I configured through Pihole) and 1 IP address (for the server, to handle the ubooquityadmin.home forwarding and in case there was ever a need to access an additional service on my server that I had not yet created a domain for).

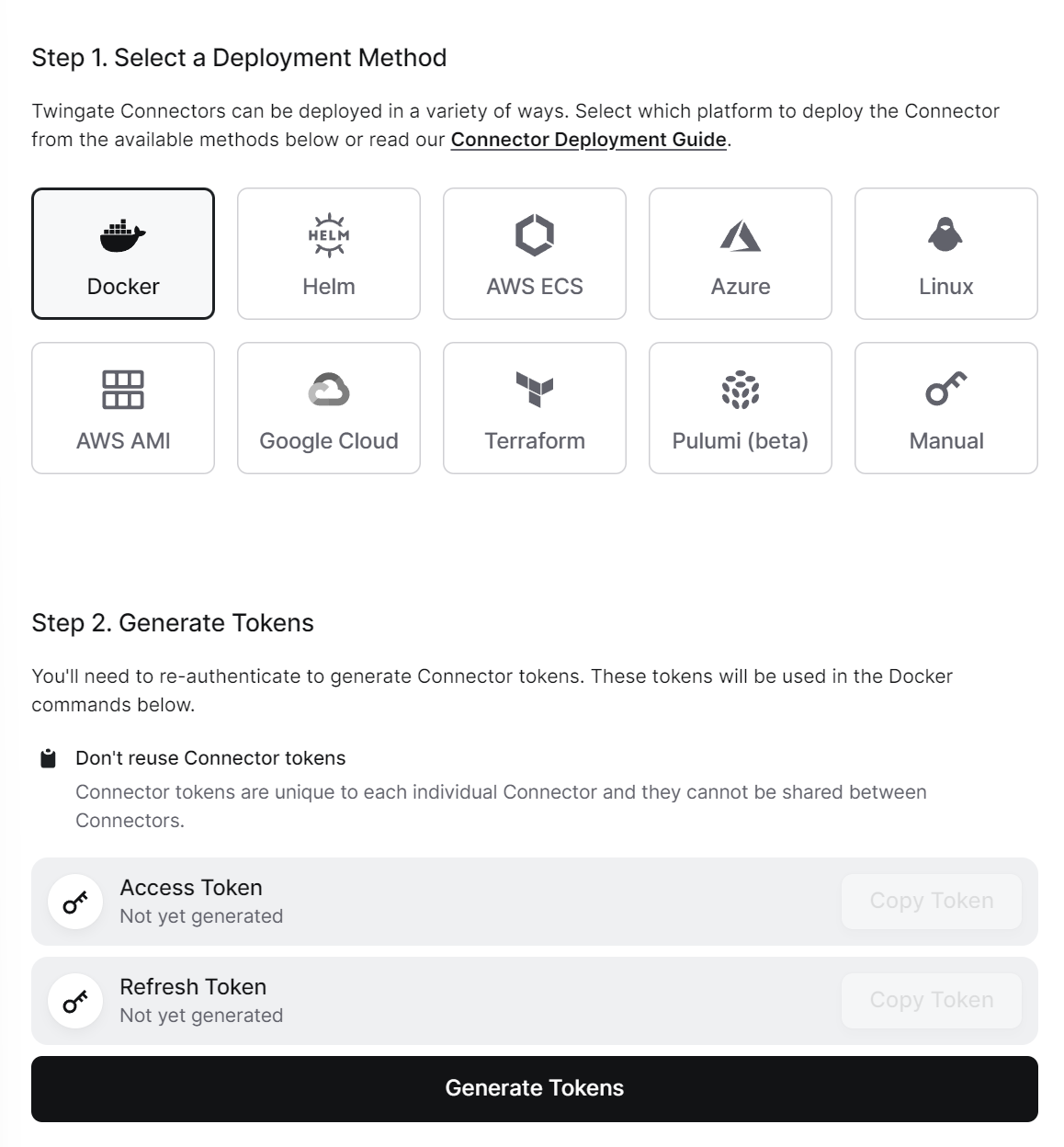

Install Connector Docker Container: To make the selected network resources available through Twingate requires installing a Twingate Connector to something internet-connected on the network.

Press the Deploy Connector button on one of the connectors on the right-hand-side of the Remote Network page (mine is called flying-mongrel). Select Docker in Step 1 to get Docker instructions (see below). Then press the Generate Tokens button under Step 2 to create the tokens that you’ll need to link your Connector to your Twingate network and resources. With the Access Token and Refresh Token saved, you are ready to configure Docker to install. Login to the OpenMediaVault administrative panel and go to [Services > Compose > Files] and press the button. Under Name put down Twingate Connector and under File, enter the following (making sure the number of spaces are consistent)

You’ll need to replace <your network name> with the name of the Twingate network you created, <your connector access token> and <your connector refresh token> with the access token and refresh token generated from the Twingate website. Do not add any single or double quotation marks around the network name or the tokens as they will result in a failed authentication with Twingate (as I was forced to learn through experience).

Once you’re done, hit Save and you should be returned to your list of Docker compose files. Click on the entry for Twingate Connector you just created and then press the (up) button to initialize the container.

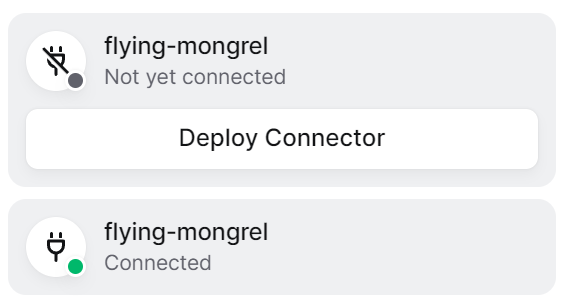

Go back to your Twingate network page and select the Remote Network your Connector is associated with. If you were successful, within a few moments, the Connector’s status will reflect this (see below for the before and after). If, after a few minutes there is still no change, you should check the container logs. This can be done by going to [Services > Compose > Services] in the OpenMediaVault administrative panel. Select the Twingate Connector container and press the (logs) button in the menubar. The TWINGATE_LOG_LEVEL=7 setting in the Docker configuration file sets the Twingate Connector to report all activities in great detail and should give you (or a helpful participant on the Twingate forum) a hint as to what went wrong.

Add Users and Install Clients: Once the configuration is done and the Connector is set up, all that remains is to add user accounts and install the Twingate client software on the devices that should be able to access the network resources.

Users can be added (or removed) by going to your Twingate network page and clicking on the Team link in the menu bar. You can Add User (via email) or otherwise customize Group policies. Be mindful of the Twingate Starter plan limit to 5 users…

As for the devices, the client software can be found at https://get.twingate.com/. Once installed, to access the network, the user will simply need to authenticate.

Remove my old VPN / Dynamic DNS setup. This is not strictly necessary, but if you followed my instructions from before, you can now undo those by:

Closing the port you opened from your Router configuration

Disabling Dynamic DNS setup from your domain provider

“Down”-ing and deleting the container and configuration file for DDClient (you can do this by going to [Services > Compose > Files] from OpenMediaVault admin panel)

Deleting the configured Wireguard clients and tunnels (you can do this by going to [Services > Wireguard] from the OpenMediaVault admin panel) and then disabling the Wireguard plugin (go to [System > Plugins])

Removing the Wireguard client from my devices

And there you have it! A secure means of accessing your network while retaining your local DNS settings and avoiding the pitfalls of Dynamic DNS and opening a port.

Resources

There were a number of resources that were very helpful in configuring the above. I’m listing them below in case they are helpful:

Stop me if you’ve heard this one before… Adoption of a technology is being impeded by too many standards. The solution? A new standard, of course, and before you know it, we now have another new standard to deal with.

The smart home industry needs to figure out how to properly embrace Thread (and Matter). It (or something like it) will be necessary for broader smart home / Internet of Things adoption.

The Thread protocol offers a robust mesh network designed to solve many of the smart home’s biggest problems. But only if everyone can agree on how to use it.

As a former “Excel monkey”, I am extremely tickled by the fact that what used to be analyst bravado about Excel skills (being able to create big spreadsheet models without touching the mouse was a big thing) is now a sport with viewers.

But it’s a testament to how powerful and versatile spreadsheets are. And how many people know what it is.

The joke in SaaS is that every SaaS product is basically competing with Excel. Well, apparently, Excel’s competing with e-sports and games now too!

This year, there’s a new wrinkle: it’s an elimination race. Every five minutes, the player with the fewest points will be eliminated until there’s only one Excel-er remaining. “We have already shot the game,” says Andrew Grigolyunovich, the founder and CEO of the Financial Modeling World Cup, the organization that oversees the event. It’s now being edited down for ESPN consumption, he says, and the whole match will come out on Friday as well. “It’s a really fun, exciting event.”

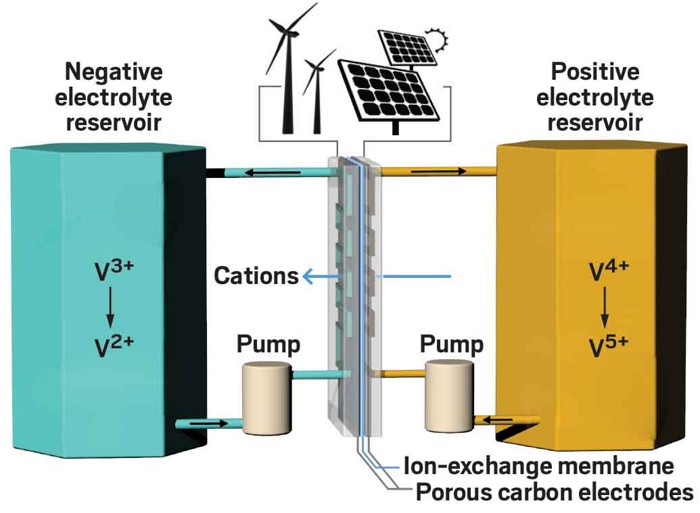

I’ve been pitched by numerous flow battery companies in my days as a deeptech/climatetech investor. The promise of the technology has always been:

Long cycle life (the number of charge-discharge cycles you can do before the performance degrades)

Easy to scale: you want 2x the storage? Just get 2x the electrolyte!

Low fire risk: most flow batteries use water-based electrolytes which won’t ignite in the air (the way the lithium in lithium-ion batteries do)

Despite compelling benefits, this category never achieved the level of success or scale as lithium-ion did. This was due in part to a variety of technological limitations (poor energy density, lower cycle efficiency, concerns around the amount of Vanadium-containing electrolyte “lying around” in a system, etc). But, the main cause was the breath-taking progress lithium-ion batteries have made in cost, energy density, and safety driven first by consumer electronics demand and then by electric vehicle demand.

This C&EN article covers the renewed optimism the flow battery world is experiencing as market interest in the technology revitalizes.

My hot-take🔥: while technological improvements play a part, once again, what is driving the flow battery market is what’s happening in lithium-ion world. There simply is too much demand for energy storage and growing uncertainty about the ability of lithium-ion to handle it in the face of the conflict between the West and China (the leading supplier of lithium ion batteries) and supply chain concerns about critical minerals for lithium ion batteries (like nickel and cobalt). Grid storage players have to look elsewhere. (Electric vehicle companies would probably like to but do not have the option!)

Considering the importance of grid energy storage in electrifying our world and onboarding new renewable generation, I think having and seeing more options is a good thing. So I, too, am optimistic here 👍🏻

Note: this is the first in a (hopefully ongoing) series of posts called “What I’m Reading” where I’ll share & comment on an interesting article I’ve come across!

Redox flow batteries have a reputation of being second best. Less energy intensive and slower to charge and discharge than their lithium-ion cousins, they fail to meet the performance requirements of snazzy, mainstream applications, such as cars and cell phones. There’s no such thing as a flow-battery Tesla.

But the companies at the International Flow Battery Forum in Prague in late June were adamant that flow batteries are now cheaper, more reliable, and safer than lithium ion in a growing number of real-world stationary energy applications. Flow-battery makers say their technology—and not lithium ion—should be the first choice for capturing excess renewable energy and returning it when the sun is not out and the wind is not blowing.

VPN — lets me connect to my storage and media server when I’m outside of my home

Until about a week ago, I had run a Plex media server on my aging (8 years old!) NVIDIA SHIELD TV. While I loved the device, it was starting to show it’s age – it would sometimes overheat and not boot for several days. My home technology setup had also shifted. I bought the SHIELD all those years ago to put Android TV functionality onto my “dumb” TV.

But, about a year ago, I upgraded to a newer Sony TV which had it built-in. Now, the SHIELD felt “extra” and the media server felt increasingly constrained by what it could not do (e.g., slow network access speeds, can only run services that are Android apps, etc.)

I considered buying a high-end consumer NAS from Synology or QNAP (which would have been much simpler!), but decided to build my own to both get better hardware for less money but also as a fun project which would teach me more about servers and let me configure everything to my heart’s content.

If you’re interested in doing something similar, let me walk you through my hardware choices and the steps I took to get to my current home server setup.

Note: on the recommendation of a friend, I’ve since reconfigured how external access works to not rely on a VPN with an open port and Dynamic DNS and instead use Twingate. For more information, refer to my post on Setting Up Pihole, Nginx Proxy, and Twingate with OpenMediaVault

Hardware

I purchased a Beelink EQ12 Mini, a “mini PC” (fits in your hand, power-efficient, but still capable of handling a web browser, office applications, or a media server), during Amazon’s Prime Day sale for just under $200.

While I’m very happy with the choice I made, for those of you contemplating something similar, the exact machine isn’t important. Many of the mini PC brands ultimately produce very similar hardware, and by the time you read this, there will probably be a newer and better product. But, I chose this particular model because:

It was from one of the more reputable Mini PC brands which gave me more confidence in its build quality (and my ability to return it if something went wrong). Other reputable vendors beyond Beelink include Geekom, Minisforum, Chuwi, etc.

It had a USB-C port which helps with futureproofing, and the option to convert this into something else useful if this server experiment doesn’t work out.

It had an Intel CPU. While AMD makes excellent CPUs, the benefit of going with Intel is support for Intel Quick Sync, which allows for hardware accelerated video transcode (converting video and audio streams to different formats and resolutions – so that other devices can play them – without overwhelming the system or needing a beefy graphics card). Many popular media servers support Intel Quick Sync-powered transcode.

It was not a i3/5/7/9 chip. Intel’s higher end chips have names that include “i3” or “i5” or “i7”. Those are generally overkill on performance, power consumption, and price for a simple file and media server. All I needed for my purposes was a lower-end Celeron-type device.

It was the most advanced Intel architecture I could find for ≤$200. While I didn’t need the best performance, there was no reason to avoid more advanced technology. Thankfully, the N100 chip in the EQ12 Mini uses Intel’s 12th Generation Core architecture (Alder Lake). Many of the other mini-PCs at this price range had older (10th and 11th generation) CPUs.

I went with the smallest RAM and onboard storage option. I wasn’t planning on putting much on the included storage (because you want to isolate the operating system for the server away from the data) nor did I expect to tax the computer memory for my use case.

I also considered purchasing a Raspberry Pi, a <$100 low-power device popular with hobbyists, but the lack of transcode and the non-x86 architecture (Raspberry Pi’s use ARM CPUs and won’t be compatible with all server software) pushed me towards an Intel-based mini PC.

In addition to the mini-PC, I also needed:

Storage: a media server / NAS without storage is not very useful. I had a 4 TB USB hard drive (previously connected to my SHIELD TV) which I used here, and I also bought a 4 TB SATA SSD (for ~$150) to mount inside the mini-PC.

Note 1: if you decide to go with OpenMediaVault as I have, install the Linux distribution before you install the SATA drive. The installer (foolishly) tries to install itself to the first drive it finds, so don’t give it any bad options.

Note 2: most Mini PC manufacturers say their systems only support additional drives up to 2 TB. This appears to be mainly the manufacturers being overly conservative. My 4 TB SATA SSD works like a charm.

A USB stick: Most Linux distributions (especially those that power open source NAS solutions) are installed from a bootable USB stick. I used one that was lying around that had 2 GB on it.

Ethernet cables and a “dumb” switch: I use Google Wifi in my home and I wanted to connect both my TV and my new media server to the router in my living room. To do that, I bought a simple Ethernet switch (you don’t need anything fancy because it’s just bridging several devices) and 3 Ethernet cables to tie it all together (one to connect the router to the switch, one to connect the TV to the switch, and one to connect the server to the switch). Depending on your home configuration, you may want something different.

A Monitor & Keyboard: if you decide to go with OpenMediaVault as I have, you’ll only need this during the installation phase as the server itself is controllable through a web interface. So, I used an old keyboard and monitor (that I’ve since given away).

OpenMediaVault

There are a number of open source home server / NAS solutions you can use. But I chose to go with OpenMediaVault because it’s:

built on Debian (a well-supported, widely used flavor of Linux)

Plug the USB stick into the mini PC (and make sure to connect the monitor and keyboard) and then turn the machine on. If it goes to Windows (i.e. it doesn’t boot from your USB stick), you’ll need to restart and go into BIOS (you can usually do this by pressing Delete or F2 or F7 after turning on the machine) to configure the machine to boot from a USB drive.

You should pick a good root password and write it down (it gates administrative access to the machine, and you’ll need it to make some of the changes below).

You can pick pretty much any name you want for the hostname and domain name (it shouldn’t affect anything but it will be what your machine calls itself).

Make sure to select the right drive for installation

And that should be it! After you complete the installation, you will be prompted to enter the root password you created to login.

Unfortunately for me, OpenMediaVault did not recognize my mini PC’s ethernet ports or wireless card. If it detects your network adapter just fine, you can skip this next block of steps. But, if you run into this, select the “does not have network card” option and “minimal setup” options during install. You should still be able to get the end of the process. Then, once the OpenMediaVault operating system installs and reboots:

Login by entering the root password you picked during the installation and make sure your system is plugged in to your router via ethernet. Note: Linux is known to have issues recognizing some wireless cards and it’s considered best practice to run a media server off of Ethernet rather than WiFi.

In the command line, enter omv-firstaid. This is a gateway to a series of commonly used tools to fix an OpenMediaVault install. In this case, select the Configure Network Interface option and say yes to all the IPv4 DHCP options (you can decide if you want to set up IPv6).

Step 2 should fix the issue where OpenMediaVault could not see your internet connection. To prove this, you should try two things:

Enter ping google.com -c 3 in the command line. You should see 3 lines with something like 64 bytes from random-url.blahurl.net showing that your system could reach Google (and thus the internet). If it doesn’t work, try again in a few minutes (sometimes it takes some time for your router to register a new system).

Enter ip addr in the command line. Somewhere on the screen, you should see something that probably looks like inet 192.168.xx.xx/xx. That is your local IP address and it’s a sign that the mini PC has connected to your router.

Now you need to update the Linux operating system so that it knows where to look for updates to Debian. As of this writing, the latest version of OpenMediaVault (6) is based on Debian 11 (codenamed Bullseye), so you may need to replace bullseye with <name of Debian codename that your OpenMediaVault is based on> in the text below if your version is based on a different version of Debian (i.e. Bookworm, Trixie, etc.).

In the command line, enter nano /etc/apt/sources.list. This will let you edit the file that contains all the information on where your Linux operating system will find valid software updates. Enter the text below underneath all the lines that start with # (replacing bullseye with the name of the Debian version that underlies your version of OpenMediaVault if needed).

deb http://deb.debian.org/debian bullseye main deb-src http://deb.debian.org/debian bullseye main deb http://deb.debian.org/debian-security/ bullseye-security main deb-src http://deb.debian.org/debian-security/ bullseye-security main deb http://deb.debian.org/debian bullseye-updates main deb-src http://deb.debian.org/debian bullseye-updates main

Then press Ctrl+X to exit, press Y when asked if you want to save your changes, and finally Enter to confirm that you want to overwrite the existing file.

To prove that this worked, in the command line enter apt-get update and you should see some text fly by that includes some of the URLs you entered into sources.list. Next enter apt-get upgrade -y, and this should install all the updates the system found.

Congratulations, you’ve installed OpenMediaVault!

Setting up the File Server

You should now connect any storage (internal or USB) that you want to use for your server. You can turn off the machine if you need to by pulling the plug, or holding the physical power button down for a few seconds, or by entering shutdown now in the command line. After connecting the storage, turn the system back on.

Once setup is complete, OpenMediaVault can generally be completely controlled and managed from the web. But to do this, you need your server’s local IP address. Log in (if you haven’t already) using the root password you set up during the installation process. Enter ip addr in the command line. Somewhere on the screen, you should see something that looks like inet 192.168.xx.xx/xx. That set of numbers connected by decimal points but before the slash (for example: 192.168.444.23) is your local IP address. Write that down.

Now, go into any other computer connected to the same network (i.e. on WiFi or plugged into the router) as the media server and enter the local IP address you wrote down into the address bar of a browser. If you configured everything correctly, you should see something like this (you may have to change the language to English by clicking on the globe icon in the upper right):

The OpenMediaVault administrative panel login

Congratulations, you no longer need to connect a keyboard or mouse to your server, because you can manage it from any other computer on the network!

Login using the default username admin and default password openmediavault. Below are the key things to do first. (Note: after hitting Save on a major change, as an annoying extra precaution, OpenMediaVault will ask you to confirm the change again with a bright yellow confirmation banner at the top. You can wait until you have several changes, but you need to make sure you hit the check mark at least once or your changes won’t be reflected):

Change your password: This panel controls the configuration for your system, so it’s best not to let it be the default. You can do this by clicking on the (user settings) icon in the upper-right and selecting Change Password

Some useful odds & ends:

Make auto logout (time before the panel logs you out automatically) longer. You can do this by going to [System > Workbench] in the menu and changing Auto logout to something like 60 minutes

Set the system timezone. You can do this by going to [System > Date & Time] and changing the Time zone field.

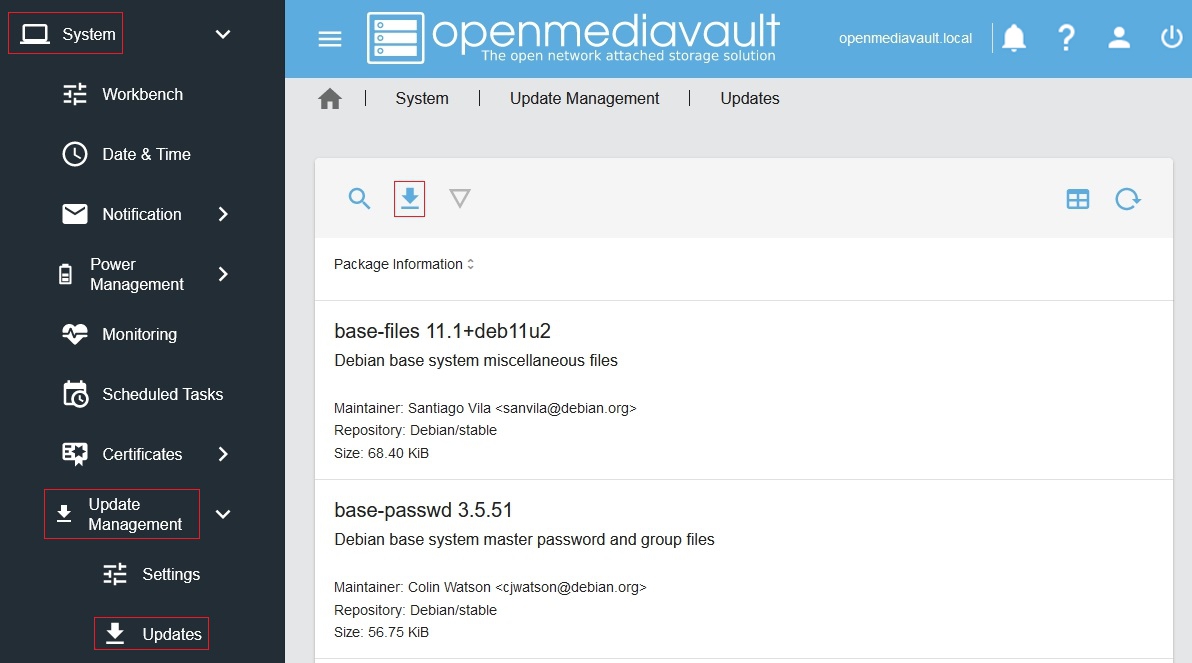

Update the software: On the left-hand side, select [System > Update Management > Updates]. Press the button to search for new updates. If any show up press the button to install everything on the list that it can. (see below, Image credit: OMV-extras Wiki)

Mount your storage:

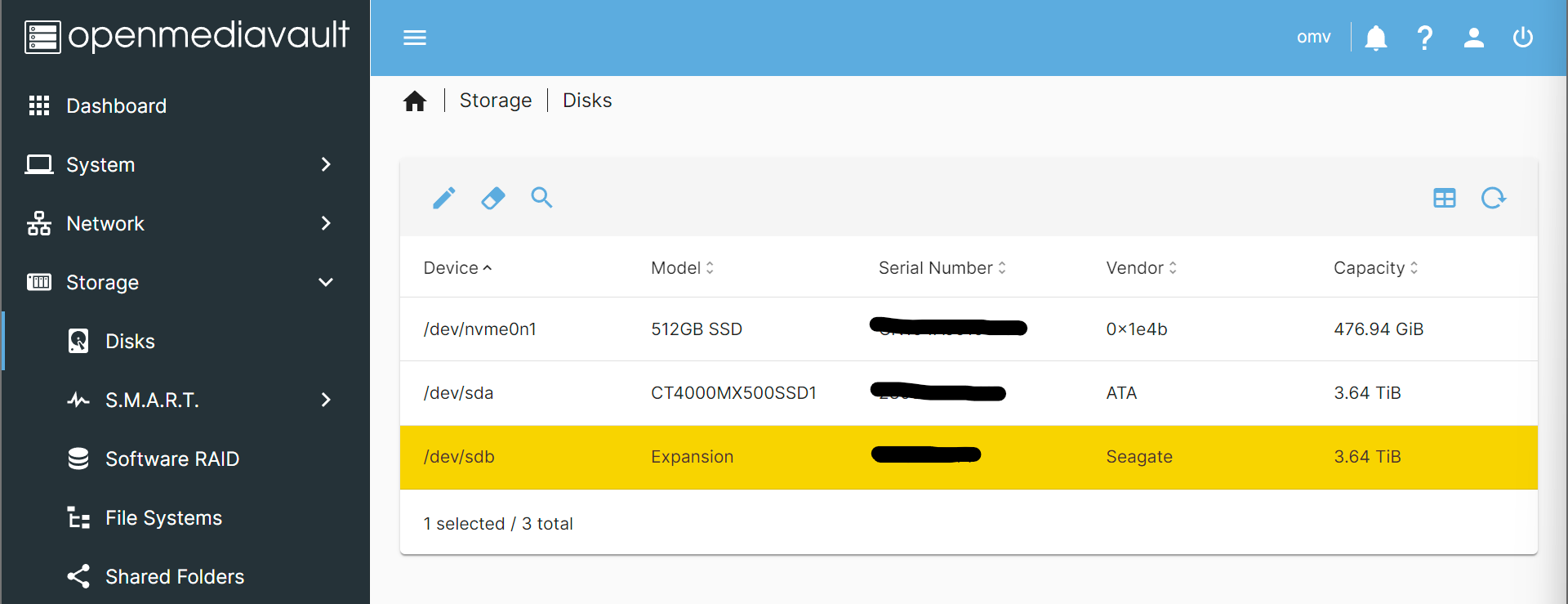

From the menu, select [Storage > Disks]. The table that results (see below) shows everything OpenMediaVault sees connected to your server. If you’re missing anything, time to troubleshoot (check the connection and then make sure the storage works on another computer).

It’s a good idea (although not strictly necessary) to reformat any un-empty disks before using them with OpenMediaVault for performance. You can do this by selecting the disk entry (marking it yellow) and then pressing the (Wipe) button

Go to [Storage > File Systems]. This shows what drives (and what file systems) are accessible to OpenMediaVault. To properly mount your storage:

Press the button for every unformatted drive added you may want to mount to OpenMediaVault. This will add a disk with an existing file system to the purview of your file server.

Press the button in the upper-left (just to the right of the triangular button) to add a drive that’s just been formatted. Of the file system options that come up, I would choose EXT4 (it’s what modern Linux operating systems tend to use). This will result in your chosen file system being added to the drive before it’s ultimately mounted.

Set up your File Server: Ok, you’ve got storage! Now you want to make it available for the computers on your network. To do this, you need to do three things:

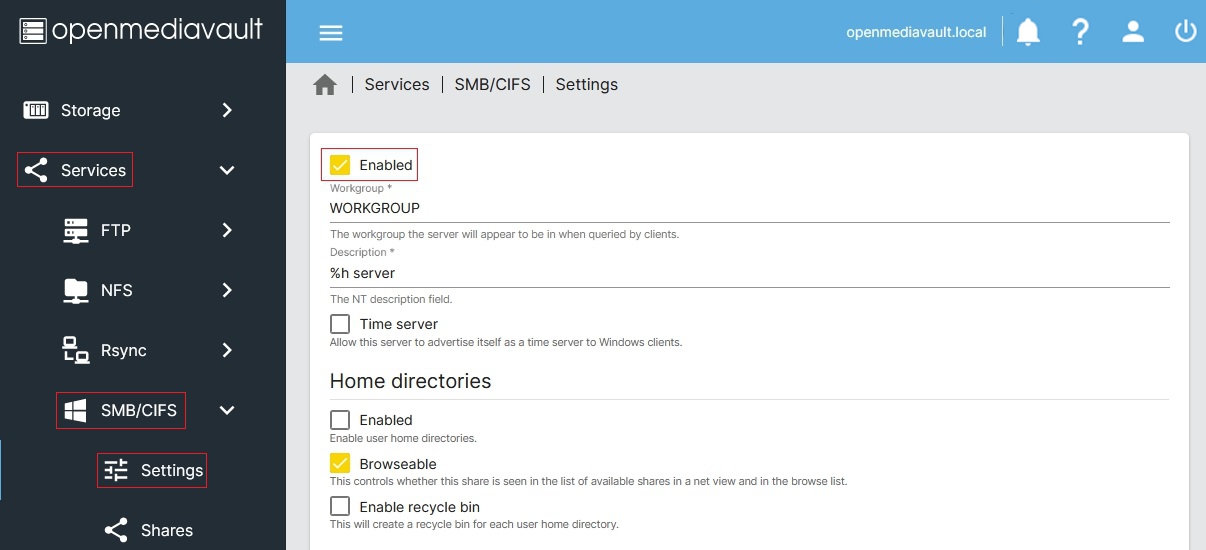

Enabling SMB/CIFS: Windows, Mac OS, and Linux systems tend to work pretty well with SMB/CIFS for network file shares. From the menu, select [Services > SMB/CIFS > Settings].

Check the Enabled box. If your LAN workgroup is something other than the default WORKGROUP you should enter it. Now any device on your network that supports SMB/CIFS will be able to see the folders that OpenMediaVault shares. (see below, Image credit: OMV-extras Wiki)

Selecting folders to share: On the left-hand-side of the administrative panel, select [Storage > Shared Folders]. This will list all the folders that can be shared.

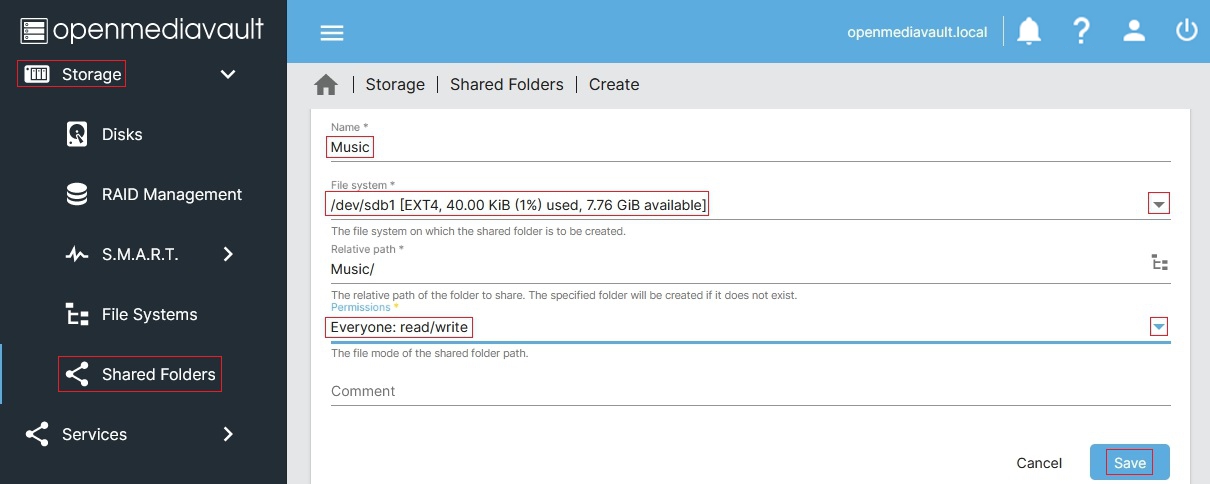

To make a folder available to your network, select the button in the upper-left, and fill out the Name (what you want the folder to be called when other’s access it) and select the File System you’ve previously mounted that the folder will connect to. You can write out the name of the directory you want to share and/or use the directory folder icon to the right of the Relative Path field to help select the right folder. Under Permissions, for simplicity I would assign Everyone: read/write. (see below, Image credit: OMV-extras Wiki)

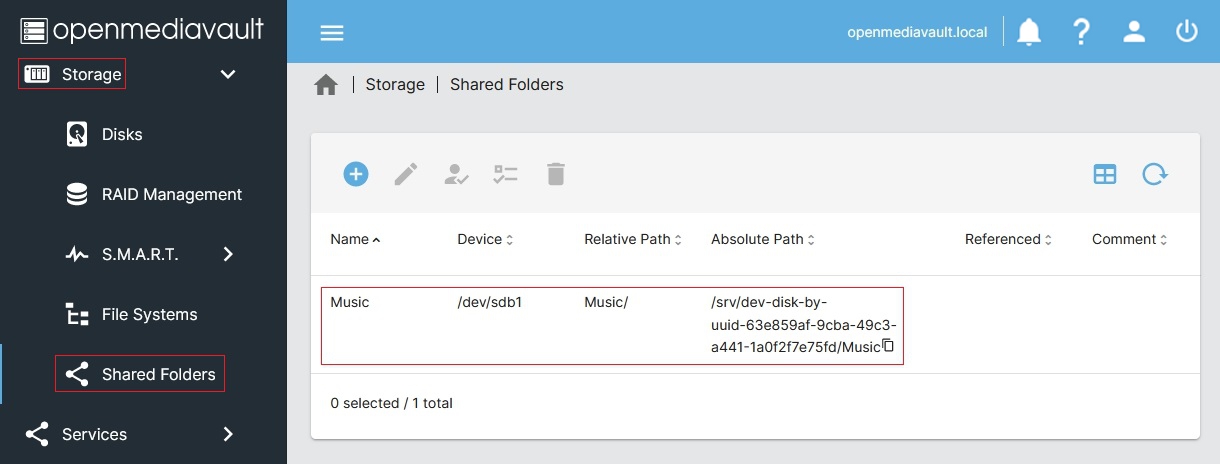

Hit Save to return to the list of folder shares (see below for what a completed entry looks like, Image credit: OMV-extras Wiki). Repeat the process to add as many Shared Folders as you’d like.

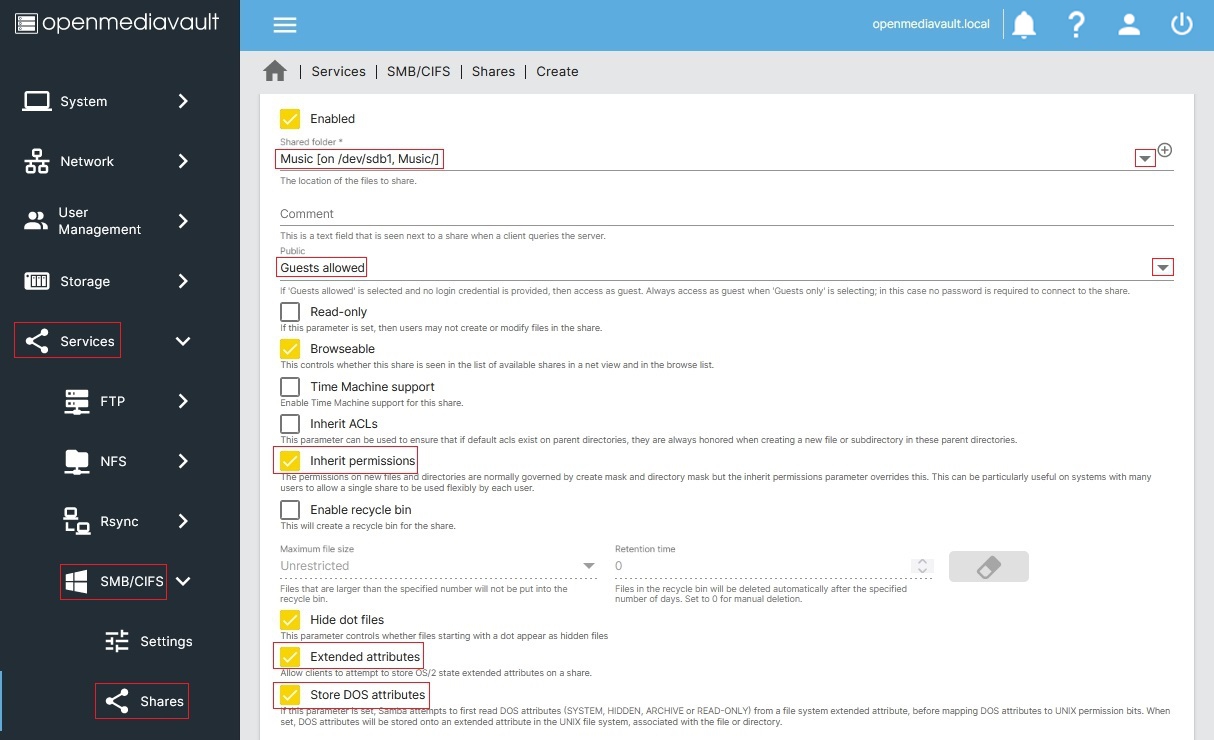

Make the shared folders available to SMB/CIFS: To do this go to [Services > SMB/CIFS > Shares]. Hit the button and, in, Shared Folder, select the Shared Folder you configured from the dropdown. Under Public, select Guests allowed – this will allow users on the network to access the folder without supplying a username or password. Check the Inherit Permissions, Extended attributes, and Store DOS attributes boxes as well and then hit Save. Repeat this for all the shared folders you want to make available. (Image credit: OMV-extras Wiki)

Set a static local IP: Home networks typically dynamically assign IP addresses to the devices on the network (something called DHCP). As a result, the IP address for your server may suddenly change. To give your server a consistent address to connect to, you should configure your router to assign a static IP to your server. The exact instructions will vary by router so you’ll need to consult your router’s documentation. In my household, we use Google Wifi and, if you do too, here are the instructions for doing so. (Make sure to write down the static IP you assign to the server as you will need it later. If you change the IP from what it already was, make sure to log into the OpenMediaVault panel from that new address before proceeding.)

Check that the shared folders show up on your network: Linux, Mac OS, and Windows all have separate ways of mounting a SMB/CIFS file share. The steps above hopefully simplify this by:

letting users connect as a Guest (no extra authentication needed)

Enter containers. Containers are “portable environments” for software, first popularized by the company Docker, that gives software a predictable background to run on. This makes it easier to run applications reliably, regardless of machine (because the application only sees what the container shows it). It also means a greatly reduced risk of a misconfigured app affecting another since the application “lives” in its own container.

While this has tremendous implications for software in general, for our purposes, this just makes it a lot easier to install software … provided you have Docker installed. For OpenMediaVault, the best way to get Docker is to install OMV-extras.

If you know how to use ssh, go ahead and use it to access your server’s IP address, login as the root user, and skip to Step 4. But, if you don’t, the easiest way to proceed is to set up WeTTY (Steps 1-3):

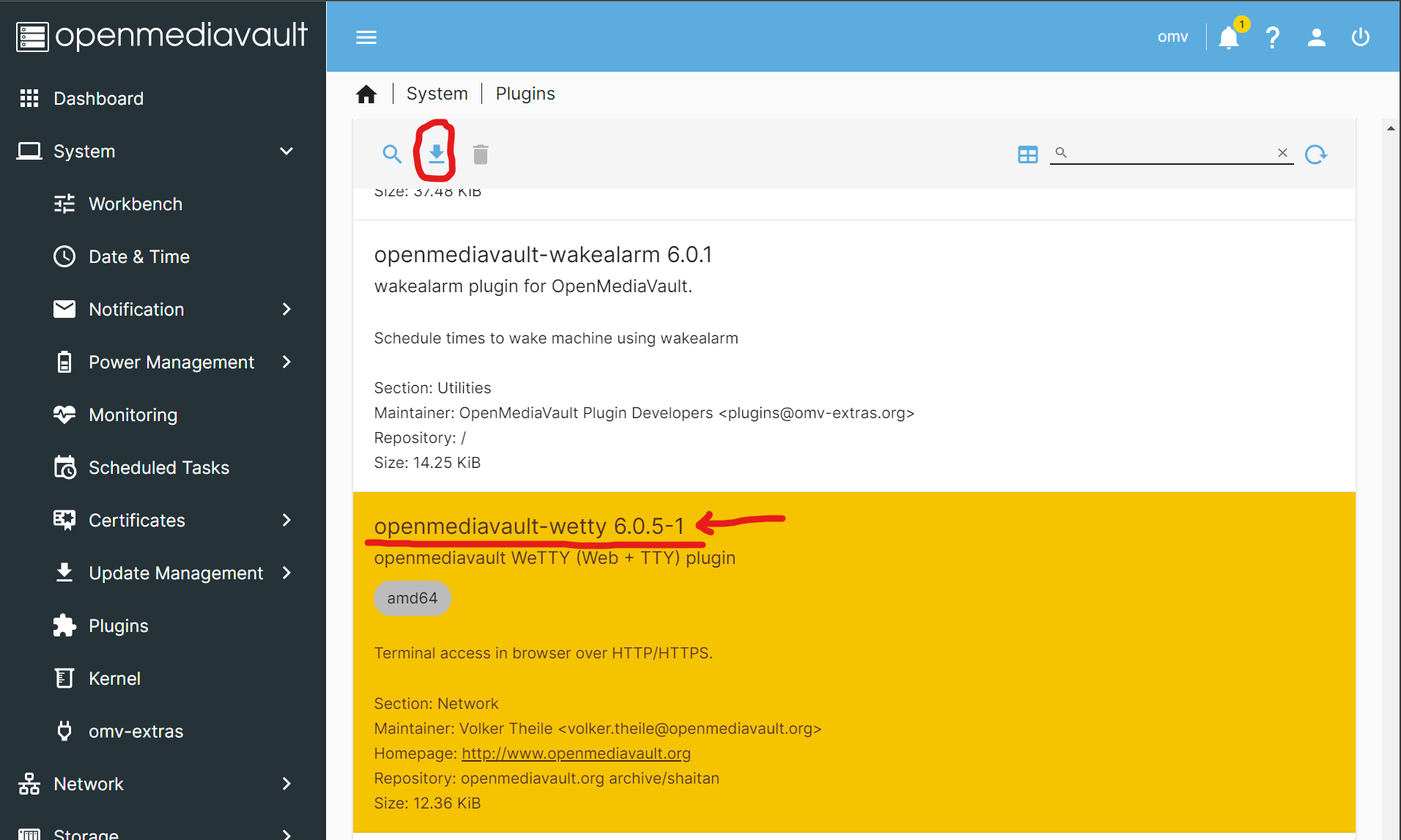

Install WeTTY: Go to [System > Plugins] and search or scroll until you find the row for openmediavault-wetty. Click on it to mark it yellow and then press the button to install it. WeTTY is a web-based terminal which will let you access the server command line from a browser.

Enable WeTTY: Once the install is complete, go to [Services > WeTTY], check the Enabled box, and hit Save. You’ll be prompted by OpenMediaVault to confirm the pending change.

Press Open UIbutton on the page to access WeTTY: It should open up a new tab that takes you to your-ip-address:2222 which should open up a black screen which is basically the command line for your server! Enter root when prompted for your username and then your root password that you configured during installation.

Installation will take a while but once it’s complete, you can verify it by going back to your administrative panel, refreshing the page, and seeing if there is a new menu item [System > omv-extras].

Enable the Docker repo: From the administrative panel, go to [System > omv-extras] and check the Docker repo box. Press the apt clean button once you have.

Install the Docker-compose plugin: Go to [System > Plugins] and search or scroll down until you find the entry for openmediavault-compose. Click on it to mark it yellow and then press the button on the upper-left to install it. To confirm that it’s been installed, you should see a new menu item [Services > Compose]

Update the System: As before, select [System > Update Management > Updates]. Press the button to search for new updates. Press the button which will automatically install everything.

Create three shared folders: compose, containers, and config: Just as with setting up the network folder shares, you can do this by going to [Storage > Shared Folders] and pressing the button in the upper left. You can generally pick any location you’d like, but make sure it’s on a file system with a decent amount of storage as media server applications can store quite a bit of configuration and temporary data (e.g. preview thumbnails).

compose and containers will be used by Docker to store the information it needs to set up and operate the containers you’ll want.

I would also recommend sharing config on the local network to make it easier to see and change the application configuration files (go to [Services > SMB/CIFS > Shares] and add it in the same way you did for the File Server step). Later below, I use this to add a custom theme to Ubooquity.

Configure Docker Compose: Go to [Services > Compose > Settings]. Where it says Shared folder under Compose Files, select the compose folder you created in Step 8. Where it says Docker storage under Docker, copy the absolute path (not the relative path) for the containers folder (which you can get from [Storage > Shared Folders]). Once that’s all set. Press Reinstall Docker.

Set up a User for Docker: You’ll need to create a separate user for Docker as it is dangerous to give any application full access to your root user. Go to [Users > Users] (yes, that is Users twice). Press the button to create a new user. You can give it whatever name (i.e. dockeruser) and password you want, but under Groups make sure to select both docker and users. Hit Save and once you’re set you should see your new user on the table. Make a note of the UID and GID (they’ll probably be 1000 and 100, respectively, if this is your first user other than the root) as you’ll need it when you install applications.

That was a lot! But, now you’ve set up Docker Compose. Now let’s use it to install some applications!

Setting up Media Server(s)

Before you set up the applications that access your data, you should make sure all of that data (i.e. photos you’ve taken, music you’ve downloaded, movies you’ve ripped / bought, PDFs you’d like to make available, etc.) are on your server and organized.

My suggestion is to set up a shared folder accessible to the network (mine is called Media) and have subdirectories in that folder corresponding for the different types of files that you may want your media server(s) to handle (for example: Videos, Photos, Files, etc). Then, use the network to move the files over (you should get comparable, if not faster, speeds as a USB transfer on a local area network).

The two media servers I’ve set up on my system are Plex (to serve videos, photos, and music) and Ubooquity (to serve files and especially ePUB/PDFs). There are other options out there, many of which can be similarly deployed using Docker compose, but I’m just going to cover my setup with Plex and Ubooquity below.

Plex

Why I chose it:

I’ve been using Plex for many years now, having set up clients on virtually all of my devices (phones, tablets, computers, and smart TVs).

I bought a lifetime Plex Pass a few years back which gives me access to even more functionality (including Intel Quick Sync transcode).

It has a wealth of automatic features (i.e. automatic video detection and tagging, authenticated access through the web without needing to configure a VPN, etc.) that have worked reliably over the years.

How to set up Docker Compose: Go to [Services > Compose > Files] and press the button. Under Name put down Plex and under File, paste the following (making sure the number of spaces are consistent)

version: "2.1" services: plex: image: lscr.io/linuxserver/plex:latest container_name: plex network_mode: host environment: - PUID=<UID of Docker User> - PGID=<GID of Docker User> - TZ=America/Los_Angeles - VERSION=docker devices: - /dev/dri/:/dev/dri/ volumes: - <absolute path to shared config folder>/plex:/config - <absolute path to Media folder>:/media restart: unless-stopped

You need to replace <UID of Docker User> and <GID of Docker User> with the UID and GID of the Docker user you created when you set up Docker Compose (Step 10 above), which will likely be 1000 and 100 if you followed the steps I laid out.

You can get the the absolute paths to your config folder and the location of your media files by going to [Storage > Shared Folders] in the administrative panel. I added a /plex to the config folder path under volumes:. This way you can install as many apps through Docker as you want and consolidate all of their configuration files in one place, while still keeping them separate.

If you have an Intel QuickSync CPU, the two lines that start with devices: and /dev/dri/ will allow Plex to use it (provided you also paid for a Plex Pass). If you don’t have a chip with Intel QuickSync, haven’t paid for Plex Pass, or don’t want it, leave out those two lines.

I live in the Bay Area so I set timezone TZ to America/Los_Angeles. You can find yours here.

Once you’re done, hit Save and you should be returned to your list of Docker compose files for the next step. Notice that the new Plex entry you created has a Down status, showing the container has yet to be initiated.

How to start / update / stop / remove your Plex container: You can manage all of your Docker Compose files by going to [Services > Compose > Files]. Click on the Plex entry (which should turn it yellow) and press the (up) button. This will create the container, download any files needed, and run it.

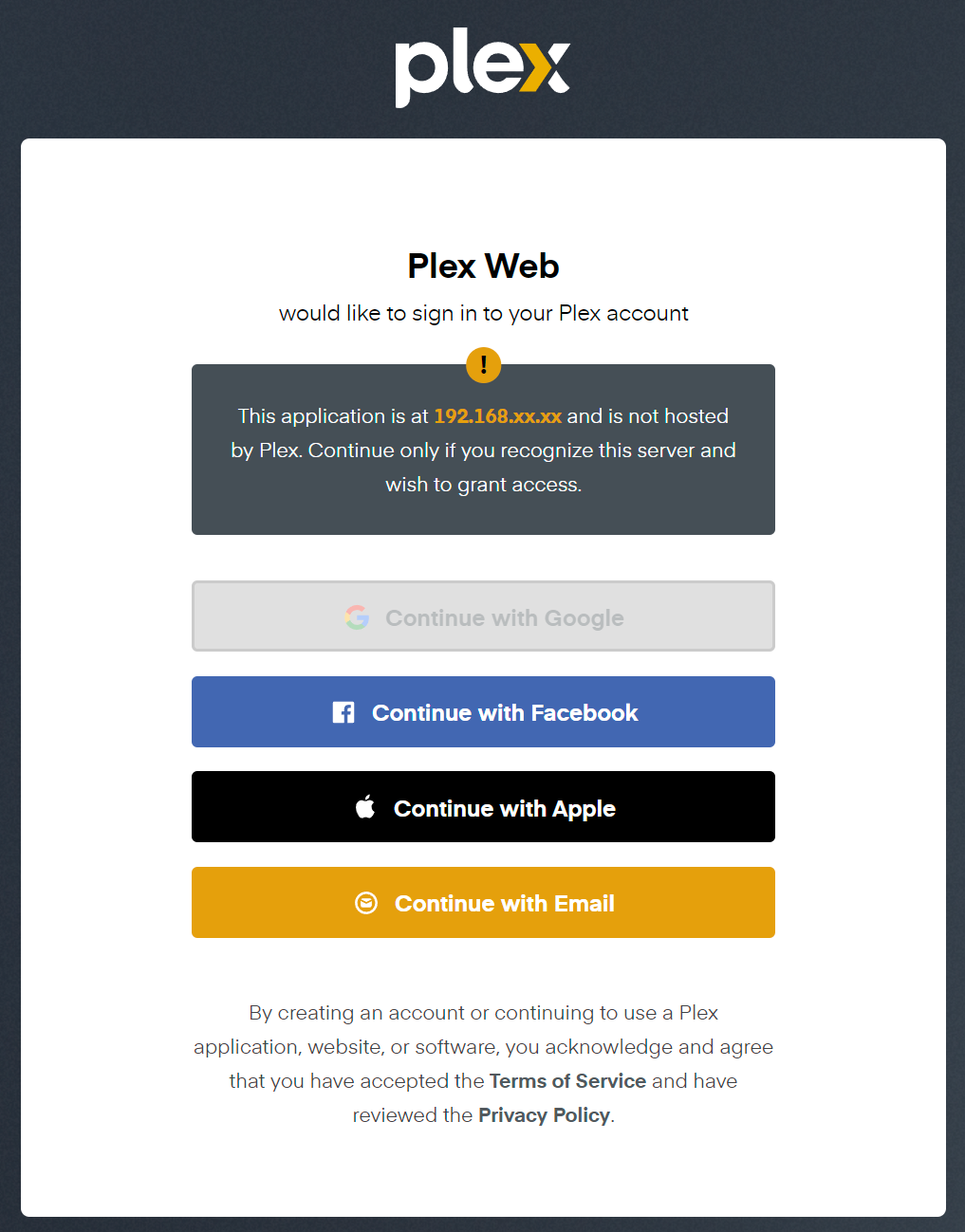

And that’s it! To prove it worked, go to http://your-ip-address:32400/web in a browser and you should see a login screen (see image below)

From time to time, you’ll want to update your software. Docker makes this very easy. Because of the image: lscr.io/linuxserver/plex:latest line, every time you press the (pull) button, Docker will pull the latest version from linuxserver.io (a group that maintains commonly used Linux containers) and, usually, you can get away with an update without needing to stop or restart your container.

Similarly, to stop the Plex container, simply tap the (stop) button. And to delete the container, tap the (down) button.

Do the setup wizard. It has good default settings (automatic library scans, remote access, etc.) — and I haven’t had to make many tweaks.

Take advantage of remote access — You can access your Plex server even when you’re not at home just by going to plex.tv and logging in.

Install Plex clients everywhere — It’s available on pretty much everything (Web, iOS, Android) and, with remote access, becomes a pretty easy way to get access to all of your content

I hide most of Plex’s default content in the Plex clients I’ve setup. While their ad-sponsored offerings are actually pretty good, I’m rarely consuming those. You can do this by configuring which things are pinned, and I pretty much only leave the things on my media server up.

Ubooquity

Why I chose it: Ubooquity has, sadly, not been updated in almost 5 years as of this writing. But, I still chose it for two reasons. First, unlike many alternatives, it does not require me to create a new file organization structure or manually tag my old files to work. It simply shows me my folder structure, lets me open the files one page at a time, maintains read location across devices, and lets me have multiple users.

Second, it’s available as a container on linuxserver.io (like Plex) which makes it easy to install and means that the infrastructure (if not the application) will continue to be updated as new container software comes out.

I may choose to switch (and the beauty of Docker is that it’s very easy to just install another content server to try it out) but for now Ubooquity made the most sense.

How to set up the Docker Compose configuration: Like with Plex, go to [Services > Compose > Files] and press the button. Under Name put down Ubooquity and under File, paste the following

--- version: "2.1" services: ubooquity: image: lscr.io/linuxserver/ubooquity:latest container_name: ubooquity environment: - PUID=<UID of Docker User> - PGID=<GID of Docker User> - TZ=America/Los_Angeles - MAXMEM=512 volumes: - <absolute path to shared config folder>/ubooquity:/config - <absolute path to shared Media folder>/Books:/books - <absolute path to shared Media folder>/Comics:/comics - <absolute path to shared Media folder>/Files:/files ports: - 2202:2202 - 2203:2203 restart: unless-stopped

You need to replace <UID of Docker User> and <GID of Docker User> with the UID and GID of the Docker user you created when you set up Docker Compose (Step 10 above), which will likely be 1000 and 100 if you followed the steps I laid out.

You can get the the absolute paths to your config folder and the location of your media files by going to [Storage > Shared Folders] in the administrative panel. I added a /ubooquity to the config folder path under volumes:. This way you can install as many apps through Docker as you want and consolidate all of their configuration files in one place, while still keeping them separate.

I live in the Bay Area so I set timezone TZ to America/Los_Angeles. You can find yours here.

Once you’re done, hit Save and you should be returned to your list of Docker compose files for the next step. Notice that the Ubooquity entry you created has a Down status, showing it has yet to be initiated.

How to start / update / stop / remove your Ubooquity container: You can manage all of your Docker Compose files by going to [Services > Compose > Files]. Click on the Ubooquity entry (which should turn it yellow) and press the (up) button. This will create the container, download any files needed, and run the system.

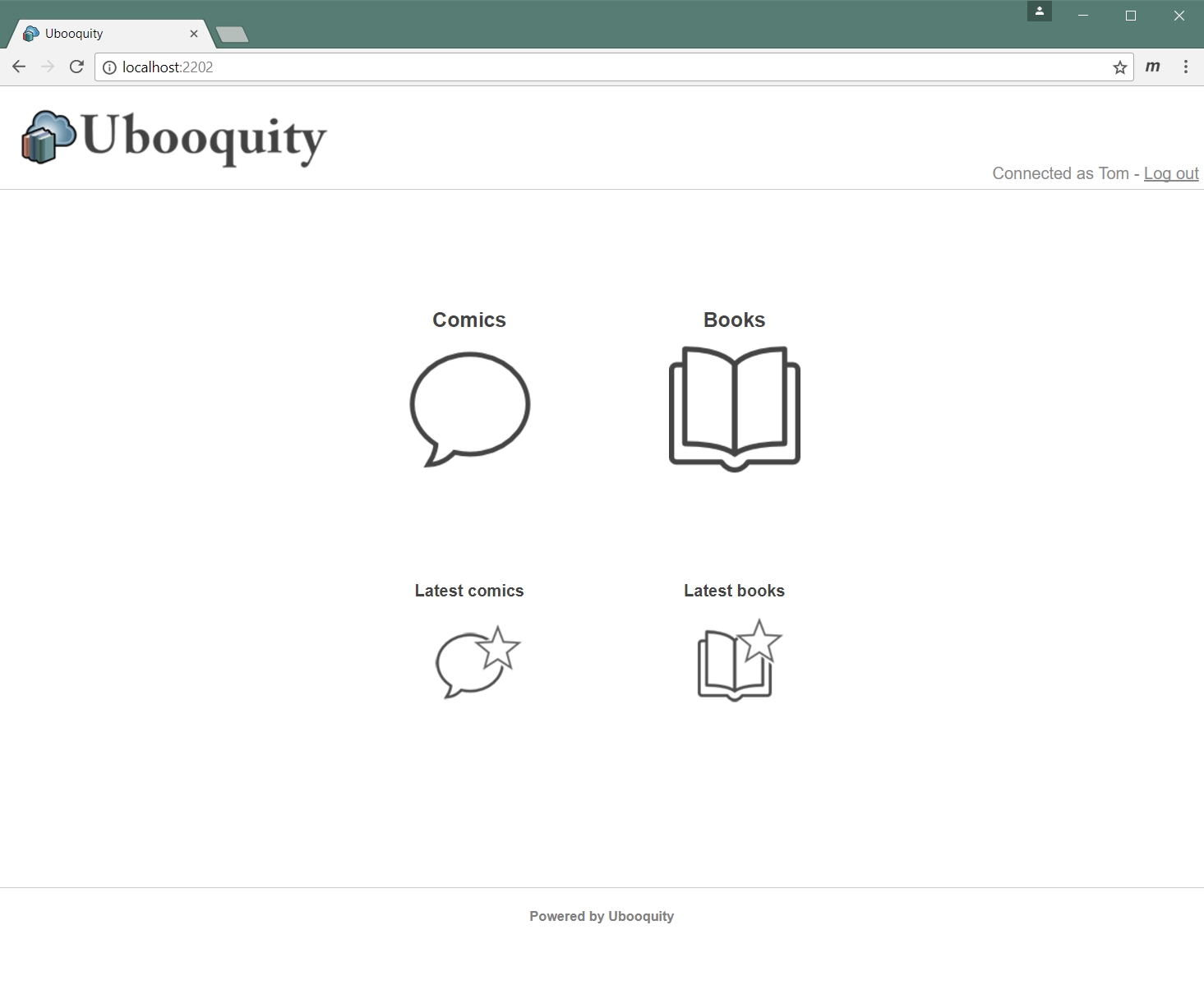

And that’s it! To prove it worked, go to your-ip-address:2202/ubooquity in a browser and you should see the user interface (image credit: Ubooquity)

From time to time, you’ll want to update your software. Docker makes this very easy. Because of the image: lscr.io/linuxserver/ubooquity:latest line, every time you press the (pull) button, Docker will pull the latest version from linuxserver.io (a group that maintains commonly used Linux containers) and, usually, you can get away with an update without needing to stop or restart your container.

Similarly, to stop the Ubooquity container, simply tap the (stop) button. And to remove the container, tap the (down) button.

Getting started with Ubooquity: While Ubooquity will more or less work out of the box, if you want to really configure your setup you’ll need to go to the admin panel atyour-ip-address:2203/ubooquity/admin (you will be prompted to create a password the first time)

In the General tab, you can see how many files are tracked in the table at the top, configure how frequently Ubooquity scans your folders for new files under Automatic scan period, manually launch a scan if you just added files with Launch New Scan, and select a theme for the interface.

If you want to create User accounts to have separate read state management or to segment which users can access specific content, you can create these users in the Security tab of the administrative panel. By doing so, you’ll need to manually go into the content type tabs (i.e. Comics, Books, Raw Files) and manually configure which users have access to which shared folders.

The easiest way to do this is to download the ZIP file at the link I gave. Unzip it on your computer (in this case it will result in the creation of a directory called plextheme-reading). Then, assuming the config shared folder you set up previously is shared across the network, take the unzipped directory and put it into the /ubooquity/themes subdirectory of the config folder.

Lastly, go back to the General tab in Ubooquity admin and, next to Current theme select plextheme-reading

Edit (10-Aug-2023): I’ve since switched to using a Local DNS service powered by Pihole to access Ubooquity using a human readable web address ubooquity.home that every device on my network can access. For information on how to do this, refer to my post on Setting Up Pihole, Nginx Proxy, and Twingate with OpenMediaVault Because entering in a local ip address and remembering 2202 or 2203 and the folders afterwards is a pain, I created keyword shortcuts for these in Chrome. The instructions for doing this will vary by browser, but to do this in Chrome, go to chrome://settings/searchEngines. There is a section of the page called Site search. Press the Add button next to it. Even though the dialog box says Add Search Engine, in practice you can use this to add keywords to any URL, just put a name for the shortcut in the Search Engine field, the shortcut you want to use in Shortcut (I used ubooquity for the core application and ubooquityadmin for the administrative console) and the URLs in URL with %s in place of query (i.e. http://your-ip-address:2202/ubooquity and http://your-ip-address:2203/ubooquity/admin).

Now to get to Ubooquity, I simply type in ubooquity in the Chrome address bar rather than a hodge podge of numbers and slashes that I’ll probably forget

External Access

One of Plex’s best features is making it very easy to access your media server even when you’re not on your home network. Having experienced that, I wanted the same level of access when I was out of the house to my network file share and applications like Ubooquity.

Edit (10-Aug-2023): I’ve since switched my method of granting external access to Twingate. This provides secure access to network resources without needing to configure Dynamic DNS, a VPN, or open up a port. For more information on how to do this, refer to my post on Setting Up Pihole, Nginx Proxy, and Twingate with OpenMediaVault

There are a few ways to do this, but the most secure path is through a VPN (virtual private network). VPNs are secure connections between computers that mimic actually being directly networked together. In our case, it lets a device securely access local network resources (like your server) even when it’s not on the home network.

OpenMediaVault makes it relatively easy to use Wireguard, a fast and popular VPN technology with support for many different types of devices. To set up Wireguard for your server for remote access, you’ll need to do six things:

Get a domain name and enable Dynamic DNS on it Most residential internet customers do not have a static IP. This means that the IP address for your home, as the rest of the world sees it, can change without warning. This makes it difficult to access externally (in much the same way that DHCP makes it hard to access your home server internally).

To address this, many domain providers offer Dynamic DNS, where a domain name (for example: myurl.com) can point to a different IP address depending on when you access it, so long as the domain provider is told what the IP address should be whenever it changes.

The exact instructions for how to do this will vary based on who your domain provider is. I use Namecheap and took an existing domain I owned and followed their instructions for enabling Dynamic DNS on it. I personally configured mine to use my vpn. subdomain, but you should use the setup you’d like, so long as you make a note of it for step 3 below.

If you don’t want to buy your own domain and are comfortable using someone else’s, you can also sign up for Duck DNS which is a free Dynamic DNS service tied to a Duck DNS subdomain.

Set up DDClient. To update the IP address your domain provider maps the domain to, you’ll need to run a background service on your server that will regularly check its IP address. One common way to do this is a software package called DDClient.

Thankfully, setting up DDClient is fairly easy thanks (again!) to a linuxserver.io container. Like with Plex & Ubooquity, go to [Services > Compose > Files] and press the button. Under Name put down DDClient and under File, paste the following

You need to replace <UID of Docker User> and <GID of Docker User> with the UID and GID of the Docker user you created when you set up Docker Compose (Step 10 above), which will likely be 1000 and 100 if you followed the steps I laid out.

You can get the the absolute path to your config folder by going to [Storage > Shared Folders] in the administrative panel. I added a /ddclient to the config folder path. This way you can install as many apps through Docker as you want and consolidate all of their configuration files in one place, while still keeping them separate.

I live in the Bay Area so I set timezone TZ to America/Los_Angeles. You can find yours here.

Once you’re done, hit Save and you should be returned to your list of Docker compose files. Click on the DDClient entry (which should turn it yellow) and press the (up) button. This will create the container, download any files needed, and run DDClient. Now, it is ready for configuration.

Configure DDClient to work with your domain provider. While the precise configuration of DDClient will vary by domain provider, the process will always involve editing a text file. To do this, login to your server using SSH or WeTTy (see the section above on Installing OMV-Extras) and enter into the command line:

nano <absolute path to shared config folder>/ddclient/ddclient.conf

Remember to substitute <absolute path to shared config folder> with the absolute path to the config folder you set up for your applications (which you can access by going to [Storage > Shared Folders] in the administrative panel).

This will open up Linux’s native text editor. Scroll to the very bottom and enter the configuration information that your domain provider requires for DynamicDNS to work. As I use Namecheap, I followed these instructions. In general, you’ll need to supply some type of information about the protocol, the server, your login / password for the domain provider, and the subdomain you intend to map to your IP address.

Then press Ctrl+X to exit, press Y when asked if you want to save, and finally Enter to confirm that you want to overwrite the old file.

Set up Port Forwarding on your router. Dynamic DNS gives devices outside of your network a consistent “address” to get to your server but it won’t do any good if your router doesn’t pass those external requests through. In this case, you’ll need to tell your router to let incoming UDP requests from port 51820 through to your server to line up with Wireguard’s defaults.

The exact instructions will vary by router so you’ll need to consult your router’s documentation. In my household, we use Google Wifi and, if you do too, here are the instructions for doing so.

Enable Wireguard. If you installed OMV-Extras above as I suggested, you’ll have access to a Plugin that turns on Wireguard. Go to [System > Plugins] on the administrative panel and then search or scroll down until you find the entry for openmediavault-wireguard. Click on it to mark it yellow and then press the button to install it.

Now go to [Services > Wireguard > Tunnels] and press the (create) button to set up a VPN tunnel. You can give it any Name you want (i.e. omv-vpn). Select your server’s main network connection for Network adapter. But, most importantly, under Endpoint, add the domain you just configured for DynamicDNS/DDClient (for example, vpn.myurl.com). Press Save

Set up Wireguard on your devices. With a Wireguard tunnel configured, your next step is to set up the devices (called clients or peers) to connect. This has two parts.

First, install the Wireguard applications on the devices themselves. Go to wireguard.com/install and download or set up the Wireguard apps. There are apps for Windows, MacOS, Android, iOS, and many flavors of Linux

Then, go back into your administrative panel and go to [Services > Wireguard > Clients] and press the (create) button to create a valid client for the VPN. Check the box next to Enable, select the tunnel you just created under Tunnel number, put a name for the device you’re going to connect under Name, and assign a unique (or it will not work) client number in Client Number . Press Save and you’ll be brought back to the Client list. Make sure to approve the change and then press the (client config) button. What you should do next depends on what kind of client device you’re configuring.

If the device you’re configuring is not a smartphone (i.e. a computer), copy the text that shows up in the Client Config popup that comes up and save that as a .conf file (for example: work_laptop_wireguard.conf). Send that file to the device in question as that file will be used by the Wireguard app on that device to configure and access the VPN. Hit Close when you’re done

If the device you’re configuring is a smartphone, hit Close button on the Client Config popup that comes up as you will be presented with a QR code that your smartphone Wireguard app can capture to configure the VPN connection.

Now go into your Wireguard app on the client device and use it to either take a picture of the QR code when prompted or load the .conf file. Your device is now configured to connect to your server securely no matter where you are. A good test of this is to disconnect a set up smartphone from your home WiFi and enable the VPN. Since you’re no longer on WiFi you should not be on the same network as your server. If you can enter http://your-ip-address in this mode into a browser and still reach the administrative panel for OpenMediaVault, you’re home free!

One additional note: by default, Wireguard also acts as a proxy, meaning all internet traffic you send from the device will be routed through the server. This can be valuable if you’re trying to access a blocked website or pretend to be from a different location, but it can also be unnecessarily slow (and bandwidth consuming). I have my Wireguard configured to only route traffic that is going to my server’s local IP address through Wireguard. You can do this by configuring your client device’s Allowed IPs to your-ip-address (for example: 192.168.99.99) from the Wireguard app.

Congratulations, you have now configured a file server and media server that you can securely access from anywhere!

Concluding Thoughts

A few concluding thoughts:

This was probably way too complicated for most people. Believe it or not, what was written above is a shortened version of what I went through. Even holding aside that use of the command line and Docker automatically makes this hard for many consumers, I still had to deal with missing drivers, Linux not recognizing my USB drive through the USB C port (but through the USB A one?), puzzling over different external access configurations (VPN vs Let’s Encrypt SSL on my server vs self-sign certificate), and minimal feedback when my initial attempts to use Wireguard failed. While I learned a great deal, for most people, it makes more sense to go completely third party (i.e. use Google / Amazon / Apple for everything) or, if you have some pain tolerance, with a high-end NAS.

Docker/containerization is extremely powerful. Prior to this, I had thought of Docker as just a “flavor” of virtual machine, a software technology underlying cloud computing which abstracts server software from server hardware. And, while there is some overlap, I completely misunderstood why containers were so powerful for software deployment. By using 3 fairly simple blocks of text, I was able to deploy 3 complicated applications which needed different levels of hardware and network access (Ubooquity, DDClient, Plex) in minutes without issue.

I was pleasantly surprised by how helpful the blogs and forums were. While the amount of work needed to find the right advice can be daunting, every time I ran into an issue, I was able to find some guidance online (often in a forum or subreddit). While there were certainly … abrasive personalities, by in large many of the questions being asked were by non-experts and they were answered by experts showing patience and generosity of spirit. Part of the reason I wrote this is to pay this forward for the next set of people who want to experiment with setting up their own server.

I am excited to try still more applications. Lists about what hobbyists are running on their home servers like this and this and this make me very intrigued by the possibilities. I’m currently considering a network-wide adblocker like Pi-Hole and backup tools like BorgBackup. There is a tremendous amount of creativity out there!

For more help on setting any of this stuff up, here are a few additional resources that proved helpful to me:

OMV Extras Wiki — probably the single best source of help I turned to in setting up OpenMediaVault, Docker Compose, and Wireguard

Section 230 of the Communications Decency Act has been rightfully called “the twenty-six words that created the Internet.” It is a valuable legal shield which allows internet hosts and platforms the ability to distribute user-generated content and practice moderation without unreasonable fear of being sued, something which forms the basis of all social media, user review, and user forum, and internet hosting services.

While I think it’s reasonable to modify Section 230 to obligate platforms to help victims of clearly heinous acts like cyberstalking, swatting, violent threats, and human rights violations, what the Democratic Senators are proposing goes far beyond that in several dangerous ways.

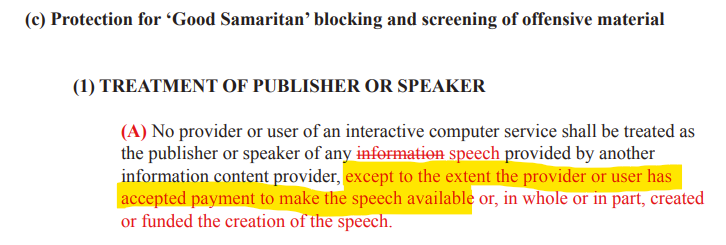

First, Warner and his colleagues have proposed carving out from Section 230 all content which accompanies payment (see below). While I sympathize with what I believe was the intention (to put a different bar on advertisements), this is remarkably short-sighted, because Section 230 applies to far more than companies with ad / content moderation policies Democrats dislike such as Facebook, Google, and Twitter.

It also encompasses email providers, web hosts, user generated review sites, and more. Any service that currently receives payment (for example: a paid blog hosting service, any eCommerce vendor who lets users post reviews, a premium forum, etc) could be made liable for any user posted content. This would make it legally and financially untenable to host any potentially controversial content.

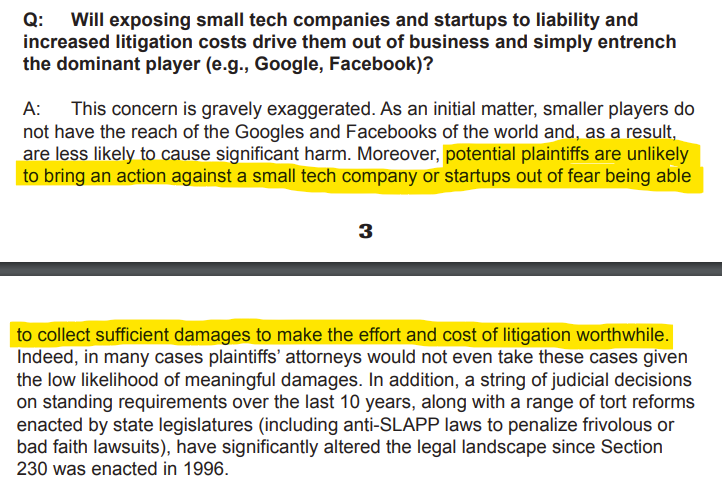

Secondly, these rules will disproportionately impact smaller companies and startups. This is because these smaller companies lack the resources that larger companies have to deal with the new legal burdens and moderation challenges that such a change to Section 230 would call for. It’s hard to know if Senator Warner’s glip answer in his FAQ that people don’t litigate small companies (see below) is ignorance or a willful desire to mislead, but ask tech startups how they feel about patent trolls and whether or not being small protects them from frivolous lawsuits

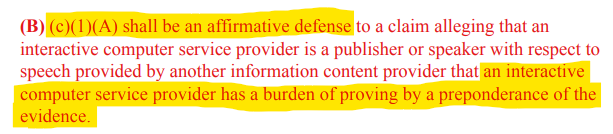

Third, the use of the language “affirmative defense” and “injunctive relief” may have far-reaching consequences that go beyond minor changes in legalese (see below). By reducing Section 230 from an immunity to an affirmative defense, it means that companies hosting content will cease to be able to dismiss cases that clearly fall within Section 230 because they now have a “burden of [proof] by a preponderance of the evidence.”

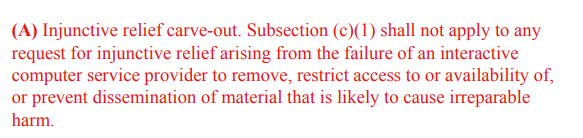

Similarly, carving out “injunctive relief” from Section 230 protections (see below) means that Section 230 doesn’t apply if the party suing is only interested in taking something down (but not financial damages)

I suspect the intention of these clauses is to make it harder for large tech companies to dodge legitimate concerns, but what this practically means is that anyone who has the money to pursue legal action can simply tie up any internet company or platform hosting content that they don’t like.

That may seem like hyperbole, but this is what happened in the UK until 2014 where libel / slander laws making it easy for wealthy individuals and corporations to sue anyone for negative press due to weak protections. Imagine Jeffrey Epstein being able to sue any platform for carrying posts or links to stories about his actions or any individual for forwarding an unflattering email about him.

There is no doubt that we need new tools and incentives (both positive and negative) to tamp down on online harms like cyberbullying and cyberstalking, and that we need to come up with new and fair standards for dealing with “fake news”. But, it is distressing that elected officials will react by proposing far-reaching changes that show a lack of thoughtfulness as it pertains to how the internet works and the positives of existing rules and regulations.

It is my hope that this was only an early draft that will go through many rounds of revisions with people with real technology policy and technology industry expertise.

Amazon’s Lightsail service has made it remarkably cheap and simple for people hosting webpages (including this blog) and simple web applications to get access to high quality virtual private servers (VPS). Beyond the ability to do really stupid things with your VPS powers, my only real complaint with the experience thus far has been that getting HTTPS working with Let’s Encrypt’s free SSL certificates has been a a hassle, requiring a lot more DNS configuration and manual command-line tweaking than is really necessary.

Manually adjusting your DNS configuration with TXT records to confirm domain ownership (each renewal)

Manually copying of certificate files to the right directory

Requires you to manually setup URL redirection (i.e. moving your HTTP URLs to HTTPS, figuring out how to handle “www.” subdomain, etc)